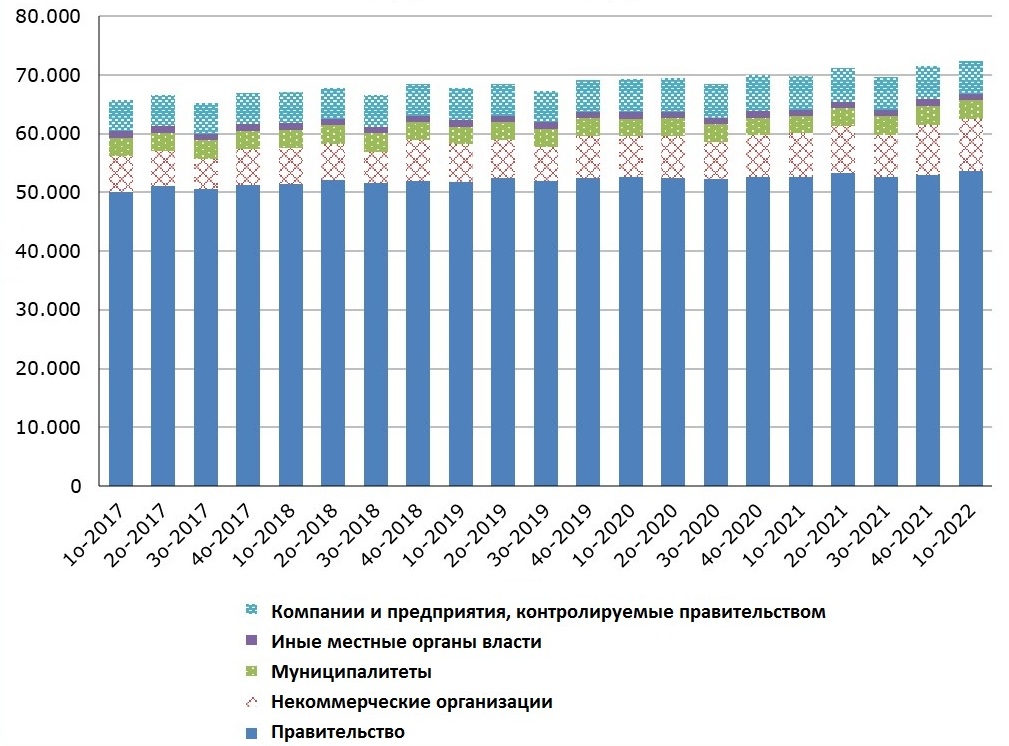

Общая численность работников в расширенном государственном секторе в первом квартале 2022 года составила 72 456 человек. В государственных ведомствах работают 66 813 госслужащих, а в компаниях и предприятиях, контролируемых правительством, так называемых полуправительственных организациях, еще 5 643 человека.

Где они работают?

В системе управления, куда относят сотрудников правительства, некоммерческих организаций и местных органов власти, занятость составила 53 655, 8 843 и 4 315 человек соответственно.

Занятость в расширенном государственном секторе в первом квартале 2017 года ― первом квартале 2022

Их стало больше

По сравнению с соответствующим кварталом 2021 года занятость в расширенном государственном секторе увеличилась на 2 637 человека (+3,8%). Увеличение наблюдалось в центральном правительственном аппарате (на 2 380 человек или 4%) и в местных органах власти (на 293 человека или 7,3%), в то время как в контролируемых государством компаниях и предприятиях произошло сокращение на 36 сотрудников (-0,6%).

По сравнению с четвертым кварталом 2021 года занятость в расширенном государственном секторе увеличилась на 893 человека (1,2%). Увеличение наблюдалось в центральном правительственном аппарате на 995 человек (+1,6%). В местных органах власти число сотрудников сократилось на 102 человека (-2,3%), в то время как в контролируемых правительством компаниях и предприятиях занятость оставалась стабильной.

В прошлом году, незаметно для абсолютного большинства предпринимателей, был принят закон, меняющий их отношения с поставщиками услуг. Теперь, нанимая самозанятого человека для выполнения какой-то разовой работы, компания должна отчислять за него взнос в соцстрах. С этим не согласился Генеральный прокурор, считая, что законодатели перепутали понятия «трудовой договор» (contract of service) и «договор об оказании услуг» (contract for services).

На прошлой неделе Верховный суд признал конституционным расширение понятия «наемный сотрудник», содержащееся в новом законе о социальном страховании и ранее вызвавшее недовольство Генерального прокурора. Как это скажется на трудовых отношениях на Кипре?

Поправки в закон о социальном страховании

Спорный вопрос касался поправок в закон о социальном страховании, принятых парламентом 23 апреля 2021 года. Цель этих изменений состояла в том, чтобы расширить термин «наемный сотрудник», защитив трудящихся и гарантировав им социальное обеспечение. Согласно поправкам, наемными сотрудниками должны считаться лица, предоставляющие услуги нанимателю по договору об оказании услуг или любому другому виду контракта вне зависимости от того, как он может называться. Достаточно того, что документ предполагает трудовые отношения между нанимателем и нанятым лицом.

Как было? Что меняется?

До настоящего момента договор об оказании услуг наниматель мог заключать и с самозанятыми лицами. По новому закону, взносы в фонд социального страхования теперь должен делать работодатель, даже если он нанимает самозанятых по договору об оказании услуг.

Положение, вызвавшее наибольшие споры, выглядит следующим образом: «Трудоустройство на Кипре лица на основании трудового договора, договора производственного обучения, договора покупки или предоставления услуг или любого другого трудового договора, независимо от его названия, при таких обстоятельствах, из которых можно сделать вывод о существовании отношений между работодателем и работником, включая трудоустройство на государственной службе».

В чем суть спора?

Позиция правительства, сформулированная Генеральным прокурором Йоргосом Саввидисом, заключалась в том, что новый закон стремится отождествить два совершенно разных по смыслу понятия: «трудовой договор» (contract of service) и «договор об оказании услуг» (contract for services).

Это, по его мнению, противоречит законодательству ЕС о проведении тендеров, превращая процедуру в отношения между работодателем и работником и нарушая букву и дух европейских директив.

Но на самом деле никто не заботился о частном секторе, вопрос был поднят, поскольку касался государственных расходов. Генеральный прокурор утверждал, что закон также нарушает статью 80.2 Конституции, поскольку он приведет к увеличению расходов государства, приравнивая поставщиков услуг к наемным работникам и превращая всех тех, кто предоставляет услуги правительству, в наемных работников. В таком случае государство будет обязано выплачивать взносы в фонд социального страхования, что повлечет за собой увеличение бюджетных расходов в нарушение Конституции. Наконец, Йоргос Саввидис заявил в Верховном суде, что закон нарушает статьи 122 и 125.1 Конституции, поскольку он включает лиц, оказывающих услуги в государственном секторе, в число наемных работников, то есть фактически в число госслужащих, в то время как компетенция назначать госслужащих, согласно Конституции, есть только у Комиссии по государственной службе.

Верховный суд не согласился. И закон вступит в силу.

Однако Верховный суд не убедили доводы Генерального прокурора, он отклонил ходатайство и признал закон соответствующим Конституции. Закон будет опубликован и вступит в силу.

В обосновании своего решения Верховный суд указывает, что преобразование отношений предоставления услуг в трудовые отношения не происходит автоматически. Закон о социальном страховании гласит, что лицо, которое предоставляло услуги по контракту на покупку услуг, также может иметь право, независимо от классификации контракта, быть признанным «наемным работником» для целей социального обеспечения, если обстоятельства работы были таковы, что можно предположить существование отношений между работодателем и работником. Верховный суд в своем постановлении отмечает, что закон не создал нового класса наемных работников и не установил новых прав.

Рассматривать будут “вручную”, каждый раз - отдельное “расследование”

Ответственным за решение вопроса о том, считается ли человек наемным работником или самозанятым лицом, будет директор Фонда социального страхования, который перед принятием решения назначает компетентных должностных лиц для проведения полного расследования.

Сроки рассмотрения отдельных решений, как всегда, не определены. В результате, стало больше бюрократических процедур, которые, как известно, занимают на Кипре месяцы, а то и годы.

Кипр поднялся на две строчки в индексе StartupBlink, в который попадают регионы, наиболее благоприятные для открытия стартапа. В рейтинге за 2022 год был оценен потенциал 1000 городов в 100 странах. Оценка проходила как для стран, так и для отдельных городов. Кипр занял 55-е место в общем страновом зачете, поднявшись с 57-го, на котором он был в 2021 году. Из 1000 городов Лимассол на 379 месте, Никосия - на 402, при этом, за год Пафос опустился с 255 на 848 место.

Эксперты StartupBlink отметили, что Республика Кипр построила свободный рынок, основанный на сфере услуг. Кипр остается известным туристическим направлением, но ему не хватает международного признания, в основном из-за отсутствия финансирования. Правительство предлагает различные инициативы для привлечения инвесторов и предпринимателей, включая налоговые льготы для инвестиционных и инновационных бизнесов. Кипрская программа выдачи виз для начинающих перспективных предпринимателей позволяет талантливым бизнесменам из третьих стран развивать свои стартапы с высоким потенциалом роста на Кипре. Остров также зарекомендовал себя как растущий центр финтеха. Здесь базируется ряд ведущих компаний в области регуляторных технологий, интернета вещей, кибербезопасности и игровой индустрии. На Кипре наблюдается рост использования технологии блокчейн, а Университет Никосии стал первым университетом в мире, который предлагает степень магистра в области цифровых валют.

Какие города мира - лучшие для развития стартапов?

StartupBlink − исследовательский центр стартапов и инноваций. В своем отчете с 2017 года он отслеживает как динамику и тенденции в сфере стартапов. Алгоритм создания рейтинга анализирует данные от глобальных партнеров, таких как Crunchbase. Также туда входят данные, собранные от десятков тысяч зарегистрированных участников на глобальной карте StartupBlink.

Вот как выглядит общемировой рейтинг городов:

А вот так распределяются места по странам:

Рейтинг городов Кипра

Впервые Лимассол стал городом с самым высоким показателем изменений, обогнав Никосию и поднявшись на 56 позиций вверх. Никосия поднялась только на 12 позиций. Аналитики отмечают, что на Кипре фактически сложилось два центра стартапов: Никосия и Лимассол. Это редкое явление, так как обычно в большинстве стран формируется единая суверенная экосистема стартапов. «Это может оказаться очень позитивным для Кипра, поскольку оба города могут подталкивать друг друга к увеличению инвестиций, в результате чего оба станут еще более сильными центрами стартапов в будущем», ― говорится в отчете.

Не так позитивно ситуация выглядит для Пафоса, который потерял свой потенциал, опустившись с 255 места на 848. Ларнака вообще исчезла из рейтинга. «Кипр еще не создал сильной экосистемы стартапов, которая может вырасти до мирового уровня, и поэтому должен стремиться к тому, чтобы импульс как Лимассола, так и Никосии продолжался, развивая их дальше для продвижения кипрской экосистемы», ― говорится в аналитической части индекса.

9 июня Парламент Кипра принял поправки в Закон о компаниях. Главное изменение – теперь небольшие компании не обязаны проходить полноценный ежегодный аудит, достаточно будет представить заключение аудитора.

Целью изменений было упрощение контроля за финансовой отчетностью компаний, оборот которых не превышает 200 тысяч евро, а общая стоимость активов не превышает 500 тыс евро. Требование предоставлять обязательную аудиторскую отчетность отменено. Теперь предприятия получили право вместо дорогостоящего аудита заказывать только справку о том, что аудитор просмотрел их финансовую отчетность и не имеет к ней замечаний.

Таким образом, Кипр снижает административную нагрузку на малые и средние предприятия, а также расходы таких предприятий на проведение аудита. Это соответствует и международным практикам (International Standard on Review Engagements 2400).

Закон содержит исключения. Например, для компаний, которые подлежат регулированию и надзору со стороны определенных независимых органов или для дочерних компаний, которые должны подготовить аудит, чтобы материнская компания могла сделать свой.

Вышеупомянутое применимо с 1 января 2023 года, а значит применяется к финансовой отчетности за 2022 год.

Согласно статистике, около 50% зарегистрированных на Кипре компаний имеют оборот менее 200 тысяч евро. Из них, 37 000 компаний (38%) имеют оборот до 100 тыс. евро, 47 000 компаний (49%) ― оборот до 200 тыс. евро.

Хотите получать деловые новости Кипра быстро и оперативно? Следить за всем, что произошло в сферах бизнеса, экономики и финансов стало еще проще.

Мы создали для вас Telegram-канал: новости сюда попадают сразу же после публикации на сайте и немедленно становятся доступны нашим подписчикам.

Важная информация сама появятся в ленте вашего телефона и вы, не отвлекаясь от повседневных задач, можете узнать все самое интересное. Все новости также доступны для обсуждения, если у вас возникли вопросы – пишите их в комментариях и мы оперативно ответим.

Как подписаться на канал? Просто перейдите по ссылке https://t.me/CyprusRussianBusiness или найдите канал в поиске Telegram по запросу @cyprusrussianbusiness.

Также напоминаем, что вы можете читать наши новости в LinkedIn по ссылке https://www.linkedin.com/company/17930778/

Цель действующего правительства и лично президента Никоса Анастасиадиса ― оживить сельские районы. Об этом напомнил министр транспорта, коммуникаций и общественных работ Яннис Карусос, который подтверждает свои слова тем фактом, что правительство выделило более 370 миллионов евро на проекты развития горных районов до 2024 года.

«Правительство Никоса Анастасиадиса в течение многих лет говорит о необходимости усиления и поддержки сельской местности. Цель самого президента ― оживить сельские районы, чтобы создать условия для привлечения молодых семей, инвесторов и предпринимателей как для постоянного проживания, так и для профессиональной деятельности», ― сказал Карусос в своем приветственном слове на фестивале «Ана-Виомата» в Доре.

Есть стратегия

Он также отметил, что для достижения этой цели в 2019 году, впервые с момента основания Республики Кипр, правительство приняло Национальную стратегию развития горных селений с целью оказания реальной и существенной поддержки горным и отдаленным районам, чтобы они могли развиваться в туристическом, культурном, социальном и экономическом плане. По его словам, неотъемлемой частью развития горных районов станет улучшение дорожной инфраструктуры, усиление доступности этих районов и их связи с городскими центрами.

Новая дорога в Троодос

Министерство транспорта, коммуникаций и общественных работ осуществляет строительство трассы Лимассол-Саиттас общей протяженностью 22,5 км, ориентировочная стоимость которой составит 198 млн евро. Напомним, реализация проекта подразумевает три этапа, работы по первому этапу начались в сентябре 2020 года и, как ожидается, будут завершены к концу 2023 года. Будет построен участок автомагистрали протяженностью около 3,7 км.

370 млн евро за три года

По словам министра транспорта, предусмотренная в бюджете сумма на три года для проектов развития сельских и горных селений превышает 370 млн евро, что на 125 миллионов евро больше, чем в 2019-2021 годах.

И еще 350 млн евро

Параллельно с этим идет реализация менее масштабных, но не менее важных проектов, о которых просили жители горных деревень. Их бюджет составляет дополнительно 350 млн евро.

Что касается продвижения горных районов в качестве туристических направлений, Карусос сказал, что правительство усилиями Подминистерства туризма намерено реализовать четыре проекта по развитию агротуризма и других форм туризма, а также увеличения посещаемости в этих районах. «С помощью целевых инициатив по продвижению местных продуктов, услуг и ресурсов, обучения и подготовки персонала, модернизации центров горных видов спорта мы укрепляем туристический бизнес и делаем селения полноценными направлениями альтернативных форм туризма», ― сказал Карусос.

Кроме того, в сотрудничестве с Министерством внутренних дел и офисом комиссара по развитию горных селений была разработана конкретная жилищная политика, с тем чтобы создать перспективы для оживления кипрской сельской местности и горных районов. «Несмотря на экономические последствия, вызванные кризисом в области здравоохранения и событиями на Украине, правительство решило поддержать покупку дома в горных районах и сельской местности, особенно для молодых пар и молодых семей», ― заключил министр транспорта.

Брюссель сформулировал свои рекомендации относительно минимального размера оплаты труда, который будет введен на Кипре. Рассматривался ли тот факт, что более 90% кипрского частного бизнеса – это микро-компании до 10 человек или малый бизнес с 10-50 сотрудниками – неизвестно. Владельцы частного бизнеса обеспокоены тем, что не смогут сохранить всех сотрудников, если будет введен обязательный минимум зарплаты, на выплату соответствующих возросших налогов просто нет средств.

В рекомендациях Еврокомиссии говорится, что минимальная зарплата в 1 000 евро значительно поможет уязвимым группам населения. В этом случае их экономическое состояние улучшится на 10%. МРОТ в размере 1 000 евро даст много преимуществ и работающим женщинам, которые смогут участвовать в рынке труда с конкурентоспособной зарплатой. Согласно отчету, необходимость для многих матерей заботиться о своих детях до трех лет не способствует сокращению разрыва в профессиональных возможностях.

ЕС назвал зарплату в 1000 евро конкурентоспособной

Ожидается, что минимальная оплата в 1 000 евро положительно повлияет на государственный бюджет, увеличив налоги и поступления по линии социального страхования, в то время как расходы на социальные пособия будут сокращены. Занятость как можно большего процента населения, которая вырастет благодаря МРОТ, имеет ключевое значение для расширения рынка труда и сокращения дефицита рабочей силы.

Издание StockWatch в конце прошлого года прогнозировало, что МРОТ составит 924 евро, однако доклад Еврокомиссии, который, конечно же, носит аналитический характер, может внести определенные коррективы в эти прогнозы.

Правительство выполнит свои обязательства

Напомним, введение минимальной заработной платы состоится несмотря на смерть министра труда Зеты Эмилианиду. На данный момент обязанности руководителя ведомства временно исполняет Яннис Карусос, глава Минтранса. Он заверил представителей профсоюзов ПЕО и СЕК в том, что задержки с МРОТ не будет. Ранее министр финансов Константинос Петридис уже заявлял, что правительство выполнит свои обязательства.

Сколько платят сейчас?

Напомним, для ограниченного числа специальностей минимальная заработная плата в настоящее время составляет 870 евро, эта сумма увеличивается до 924 евро, если работник имеет шесть месяцев непрерывного стажа у одного и того же работодателя.

Что думают работодатели?

На введение МРОТ с большой долей скепсиса смотрят работодатели. Глава отдела трудовых отношений Торгово-промышленной палаты Кипра Эмилиос Михаил уточнил: при том, что Торгово-промышленная палата в целом не возражает против введения минимальной заработной платы, ее руководство ждет от Минтруда пояснений по ряду острых вопросов. Определенные опасения по поводу введения МРОТ выразили и представители Федерации работодателей и промышленников. Представители федерации попросили отложить введение этой меры до тех пор, пока экономическая ситуация в стране не нормализуется. В целом работодатели поддерживают идею менять размер МРОТ в зависимости от экономической ситуации.

Что думают работники?

Исследование в ноябре прошлого года показало, что девять из десяти респондентов уверены: введение МРОТ повысит социальную защищенность трудящихся от неоправданно низких зарплат и создаст условия для достойного уровня жизни.

9 июня управляющий совет Европейского центробанка соберется, чтобы обсудить возможность повышения ключевой ставки— впервые с 2011 года. О такой перспективе уже заявила председатель ЕЦБ Кристин Лагард.

На практике это означает повышение ставок по кредитам. Издание «Филелефтерос» приводит примеры того, как изменятся суммы выплат для заемщиков, взявших кредит с плавающей ставкой. В случае ключевой процентной ставки также вырастет Европейская межбанковская ставка предложения, известная как EURIBOR.

Ипотечные кредиты

Для ипотечного кредита в размере 200 000 евро с обеспечением и сроком погашения 20 лет средняя процентная ставка сегодня составляет 2,3%, а сумма ежемесячной выплаты — 1 040 евро. Если процентная ставка увеличится на 0,25% и станет 2,55%, то взнос составит 1 064 евро. Если процентная ставка увеличится на 0,5%, то ежемесячный взнос составит уже 1 089 евро. При ипотечном кредите в размере 350 000 евро взнос с текущей процентной ставкой 2,3% составляет 1 820 евро. В случае увеличения на 0,25% взнос по кредиту вырастет до 1 863 евро, а в случае увеличения на 0,5% ежемесячный взнос увеличивается до 1 906 евро.

Бизнес-кредиты с залогом

В случае обеспеченного бизнес-кредита на сумму 200 000 евро средняя переменная рыночная ставка составляет 3,1%, а ежемесячный взнос 1 119 евро, в случае увеличения на 0,25% процентная ставка составит 3,35%, а ежемесячный взнос — 1 144 евро. В случае увеличения на 0,5% процентная ставка будет увеличена до 3,6%, а сумма взноса составит 1 170 евро.

Бизнес-кредиты без залога

Для бизнес-кредита без залога средняя рыночная ставка составляет 4,6%. Для кредита в размере 200 000 евро ежемесячный взнос составляет 1 276 евро, при увеличении на 0,25% процентная ставка становится 4,85%. Ежемесячный взнос увеличивается до 1 303 евро, а при увеличении процентной ставки на 0,5% взнос становится 1 330 евро.

Потребительские кредиты

Для потребительского кредита в размере 200 000 евро с обеспечением средняя рыночная ставка составляет 3,31%. Ежемесячный взнос будет примерно 1 140 евро. В случае увеличения процентной ставки на 0,25% взнос оценивается в 1 166 евро, а в случае увеличения на 0,5% он увеличивается до 1 192 евро.

В банках вздохнут с облегчением?

Предприятиям и домашним хозяйствам следует лучше планировать свои расходы, чтобы они могли справиться с небольшим повышением процентных ставок. Зато у банков есть все основания вздохнуть с облегчением, поскольку стресс от отрицательных процентных ставок по депозитам исчезнет, что частично отразится на их балансах. Большинство кредитов, выданных банками, имеют переменную процентную ставку или в течение первых лет фиксированную, а затем плавающую. В случае повышения процентных ставок ожидается, что они увеличат свои доходы при одновременном сокращении своих потерь от отрицательных процентных ставок.

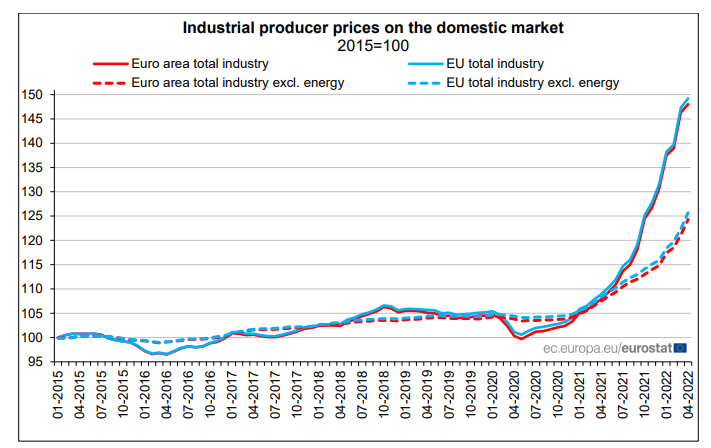

Стоимость производства растет не по месяцам, а, буквально, по дням. В период с 2011 по 2021 накопленный рост цен по странам Европы был равен нулю. В 2015 и в 2020 была даже дефляция. В итоге с 2015 по 2021 цены выросли в среднем на 5%, а сейчас некоторые страны показали рост в 30% всего за полгода.

Инфляционное давление уже превышает пики 1970-х годов и очевидно подхватывает период гиперинфляции 20-х годов прошлого века.

В целом по ЕС промежуточная продукция выросла на 25,4%, стоимость производства электроэнергии почти удвоилась, капитальные товары +7,5%, долгосрочные потребительские товары +9,1%, краткосрочные потребительские товары +12%. Вот по последним двум можно делать явную проекцию на индекс потребительских цен.

Когда «рванёт» в ЕС?

Среднее время трансмиссии производственных цен в потребительские составляет 4-5 месяцев, поэтому с июля начнет раскручиваться и потребительская инфляция, так как производственные цены уже с декабря превышают все предыдущие максимумы.

На графике наглядно показано, насколько все отклоняется от нормы.

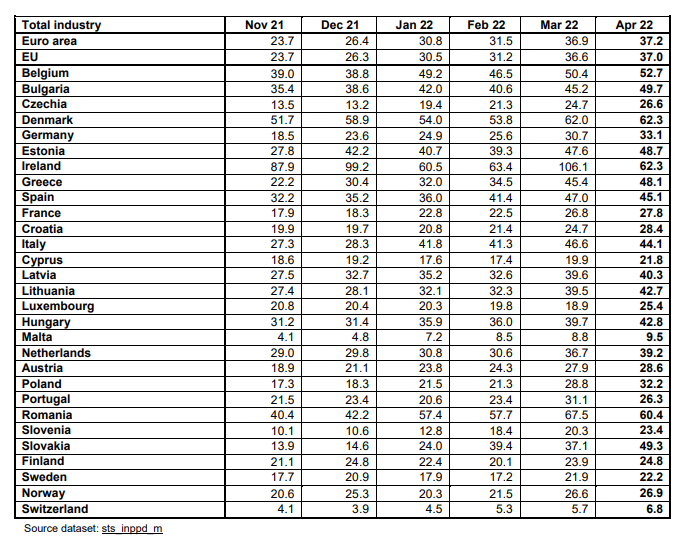

Кипр держится, но это ненадолго

Из стран ЕС только Мальте удалось удержать рост цен в пределах 10%. Кипр тоже пока неплохо справляется, находясь в середине списка с 21% по росту цен.

Снижение уровня инфляции начнется только в середине 2023 года. Все это время цены продолжат расти. Такое заявление сделали на конференции «Экономические перспективы на 2022 год». Секрет для скорейшего преодоления трудностей – поддержка среднего класса.

На Кипре реальная покупательная способность домохозяйств снижается быстрыми темпами, при этом усиливается неравенство в доходах между сотрудниками государственного и частного секторов. А поскольку уровень инфляции для работников с низким доходом, например, работников сектора розничной торговли, зарабатывающих в среднем 1250 евро в месяц, в настоящее время составляет более 10%, эти граждане потеряли более 500 евро в покупательной способности в первой половине 2022 года.

Когда в начале октября 2021 года в парламенте представляли бюджет на 2022 год, уже рост потребительских цен, стоимости сырья и топлива из-за глобального дефицита поставок был очевиден. Однако министр финансов Константинос Петридис уверял: это временное явление. Он оптимистично основывал бюджетные оценки на прогнозе – цены в стране вырастут всего на 1,5%. Поскольку правительство изначально прогнозировало, что его общие расходы сократятся в 2022 году благодаря сворачиванию помощи для предприятий, пострадавших от пандемиии, не было предпринято никаких усилий для увеличения налоговых поступлений. Однако цены и издержки продолжали расти, а с началом событий на Украине и принятием санкционных пакетов просто взлетели. Следовательно, бюджетная смета правительства на 2022 год в настоящее время выглядит не соответствующей действительности. Страна нуждается в подготовке экономики и населения к стремительной инфляции.

Действительно, учитывая, что более бедные домохозяйства тратят большую часть своего дохода на продукты питания и энергоносители, в настоящее время они сталкиваются с темпами роста расходов, значительно превышающими 10%. Кроме того, многие работодатели в частном секторе также страдают от значительного увеличения затрат на материалы и электричество. По оценкам строительных компаний, цены на стройматериалы выросли на 24,5% за 12 месяцев (с апреля 2021 до апреля 2022 года). Цены на металлические изделия выросли на 42,4%, а на изделия из дерева – на 26,5%.

В частном секторе всё хуже и хуже

Неспособность большого числа домохозяйств справиться с обострившимся кризисом объясняется относительно низкими доходами многих работников частного сектора. Кипр придерживается бизнес-модели, способствующей развитию таких секторов, как массовый туризм и строительство. При этом работа в таких ведущих секторах экономики, как гостиничная сфера, общепит, строительство, розничная торговля не требует высокой квалификации и плохо оплачивается. Кроме того, после финансового кризиса 2012-2013 годов работники в этих секторах имели мало возможностей для того, чтобы восстановить своё благосостояние. В результате они столкнулись со снижением доходов, которые резко упали в реальном выражении за последние два года. Среднемесячная заработная плата работников частного сектора в 2021 году оценивалась в 1 750 евро. На деле же две трети сотрудников частного сектора в перечисленных выше отраслях получают менее 1500 евро. Это примерно вдвое меньше, чем у государственных служащих.

Количество зарегистрированных безработных на Кипре сократилось до самых низких отметок за последние 14 лет. Об этом сообщает Статистическая служба Кипра.

Согласно данным, представленным региональными отделениями Департамента труда, число зарегистрированных безработных на конец мая 2022 года составляет 10 586 человек. Это самый низкий показатель за период с ноября 2008 года. По сравнению с маем 2021 года произошло сокращение на 20 701 человек или 66,2%.

Почему безработных стало меньше?

Это снижение в основном связано с возобновлением более или менее полноценного функционирования гостиничного сектора и общественного питания: в этой сфере количество безработных снизилось на 5 091 человек. Больше людей стали работать в сфере розничной торговли, число безработных снизилось там на 4 052 человека. Безработица также сократилась в строительном секторе (на 1 396 безработных), обрабатывающей промышленности (на 1 268 человек), секторе транспорта и хранения (на 993 человека). На 1 617 человек стало меньше безработных среди новозарегистрированных участников рынка труда.

Кто ещё ищет работу?

Наибольшее число зарегистрированных безработных по секторам в мае 2022 года было в оптовой и розничной торговле (1 950 человек безработных). Определенная безработица сохранялась в гостиничном секторе и сфере общепита (1 376 человек) и строительства (977 человек).

Рекордно низкие показатели

Согласно данным Евростата, опубликованным 1 июня, уровень безработицы на Кипре снизился с 8,4% в апреле 2021 года до 5,4% в апреле этого года. Это самый низкий показатель за 14 лет.