Увлекательное повествование из архива «Успешного бизнеса»* о том, как появилось банковское дело и как эволюционировали банки с древних времен до наших дней.

Являясь «кровеносной системой» мировой экономики, банки обеспечивают нормальное функционирование предприятий, осуществляют товарно-денежные операции, проводят платежи и расчеты, выдают кредиты и т.п. Современный банк – это центр мировой экономики.

Само слово «банк» произошло от итальянского «banco», что в переводе означает стол, на котором средневековые менялы раскладывали монеты. Слово появилось в средние века, так как в этот период банки являлись, преимущественно, меняльными конторами.

Свод законов Хаммурапи, первый кодекс законов древней Месопотамии (1754 г. до н.э.)

Возникновение банков

Первые «деньги» в виде скота, зерна, меха, кож появились на Древнем Востоке примерно за три тысячи лет до нашей эры. Местом хранения денег в то время стали храмы (культовые сооружения) как наиболее надежные и пользующиеся всеобщим доверием.

Храмы выполняли функции хранения денег и регулирования денежного обращения.

Последнее требовало выполнения учетной и расчетной операций, восстановления испорченных денег.

Постепенно общество перешло на металлические деньги (в основном серебро и золото).

Развитие товарных отношений вызвало появление платного денежного кредита и развитие кредитных операций. Одновременно появились и прототипы современных депозитов. Так постепенно древние прообразы банков стали выполнять функции хранения и накопления средств, посредничества в кредите, осуществления платежей, восстановления денег.

Храмы играли роль банков не только на Древнем Востоке, но и позже в Древней Греции, Древнем Риме и средневековой Европе.

Монеты Древнего Рима (41-54 гг.)

Децентрализация денежного обращения

Стремясь усилить свою роль в экономике, древние государства с VII века до н.э. начали сами чеканить монеты, потеснив в их производстве храмы.

В VII-V веках до н.э. в Вавилоне появились крупные торговые дома, выполнявшие разнообразные операции по купле-продаже и финансированию сделок. Это были выдача ссуд под расписку и залог, продажи и платежи за счет клиентов, финансирование сделок вкладчика, разного рода посредничество.

В то же время на Древнем Востоке появились так называемые тамкары – государственные торговые агенты. Тамкары создавали торговые общины со страховым фондом. Торговые общины в основном занимались куплей-продажей металлических денег в виде слитков. Причем тамкары и их помощники были в основном рабами, но с большими правами, соответствовавшими их богатству. Это показывает, что торгово-обменная деятельность в то время считалась делом, недостойным свободных граждан.

В Древней Греции роль тамкаров играли рабы-трапезиты (в переводе с древнегреческого – «человек за столом»). Развитие экономики Древней Греции, множество независимых городов, чеканивших свои деньги, требовали упорядочения товарно-денежных отношений. И для этого нужны были профессионально подготовленные люди. Поэтому происходил массовый захват и завоз греками рабов, знающих денежные операции.

Одни трапезиты специализировались на приеме вкладов и платежах за счет клиентов, другие выдавали под залог ссуды, третьи занимались меняльным делом.

Особенно выгодным для них делом была купля-продажа монет разных государств (в Древней Греции монеты чеканили 1 136 городов-полисов).

В государственных хранилищах Древней Греции профессиональная специализация существенно возросла. Здесь принимали и выдавали деньги, считали доходы и расходы, собирали денежные средства, оценивали правильность осуществления денежных операций, решали в судах вопросы по неверной отчетности разные специалисты.

Продолжение следует.

* Эта статья из архива «Успешного бизнеса» была впервые опубликована в январе 2015 г. Обращаем ваше внимание, что с момента написания текста могли произойти изменения, либо часть информации могла устареть.

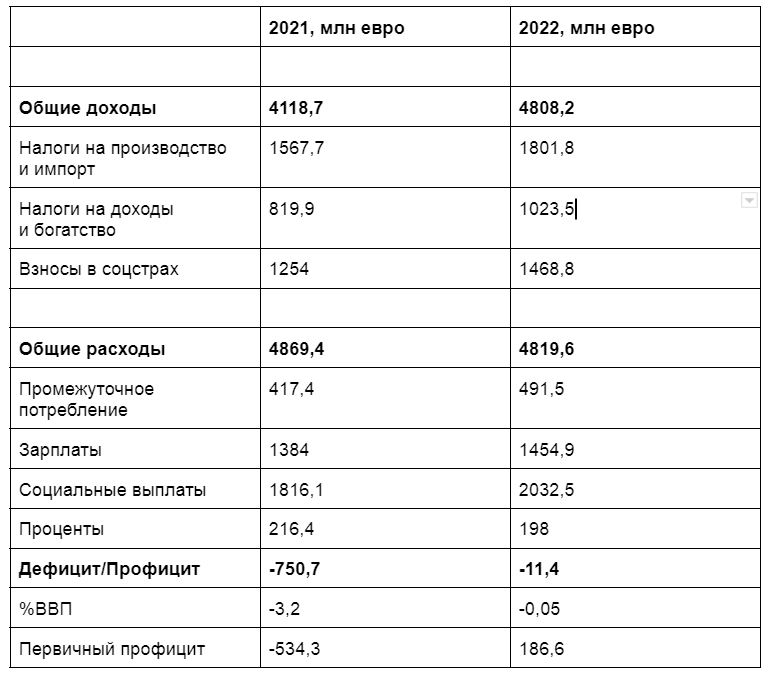

По итогам первого полугодия 2022 года на счетах правительства зафиксирован дефицит бюджета, несмотря на двузначный рост доходов. Предварительные финансовые результаты, подготовленные Статистической службой за период с января по июнь 2022 года, показывают общий дефицит госбюджета в размере 11,4 млн евро (0,05% ВВП).

Лучше, чем в прошлом году

Впрочем, этот показатель намного ниже прошлогодних цифр, так как в период с января по май 2021 года дефицит составлял 750,7 млн евро (3,2% ВВП).

Общая выручка за период с января по июнь 2022 года увеличилась на 689,5 млн евро (+16,7%), составив 4,8 млрд евро. Для сравнения, за аналогичный период 2021 года выручка составляла 4,12 млрд евро.

За счет чего увеличилась выручка?

В частности, доход от налогов на производство и импорт в первое полугодие 2021 года составлял 1,57 млрд евро, а в первом полугодии 2022 увеличился на 234,1 млн евро (+14,9%) и составил 1,8 млрд евро. Из них чистый доход от НДС (после вычета возмещений) увеличился на 192 млн. евро. (+19%) и составил 1,2 млрд евро. Поступления от налога на доходы и имущество увеличились на 203,6 млн евро. (+24,8%) и составили 1,02 млрд евро. Социальные взносы увеличились на 214,8 млн. евро (+17,1%), составив 1,47 млрд евро. Доходы от услуг увеличились на 58 млн евро (+23%), дав бюджету 310,7 млн евро. Полученные проценты и дивиденды увеличились на 15,5 млн евро (+27,7%) и принесли казне 71,5 млн евро. Напротив, капитальные трансферты сократились на 31,8 млн евро (-45%), ограничившись 38,9 млн евро. Текущие трансферты сократились на 4,7 млн евро (-4,8%), принеся казне 93 млн. евро.

Тратить стали меньше

Общие расходы в период с января по июнь 2021 года составляли 4,87 млрд евро, а в тот же период 2022 года сократились на 49,8 млн евро (-1%), составив 4,82 млрд евро. Субсидии были сокращены на 438 млн евро, до 38,2 млн евро. В первое полугодие 2021 года государство выплатило субсидий на 476,2 млн евро. Выплаченные проценты сократились на 18,4 млн евро (-8,5%), ограничившись 198 млн евро. Напротив, социальные пособия увеличились на 216,4 млн евро (+11,9%) и составили 2,03 млрд евро. Заработная плата персонала выросла на 70,9 млн евро (+5,1%), дав показатель в 1,45 млрд евро. Промежуточное потребление увеличилось на 74,1 млн евро (+17,7%) и составило 491,5 млн евро.

В таблице – нагляднее

Наглядно эти данные в сравнении с прошлым годом представлены в таблице:

2 августа власти объявили о начале приема заявок на субсидию, которая покроет установку на территории частного дома фотоэлектрической станции для подзарядки электромобиля или плагин-гибридного автомобиля. План имеет обратную силу: на субсидию могут рассчитывать те жители, которые самостоятельно установили систему для подзарядки после 1 февраля этого года.

Потенциальные бенефициары этого вида госпомощи – владельцы электрокара, живущие в собственном доме. При условии, что счет на электричество приходит на их имя, а также ближайшие родственники таких лиц, которые проживают вместе с ними и пользуются электромобилем. О программе впервые было объявлено 20 апреля, ее бюджет составляет 1,5 млн евро.

Дополнительные бонусы

Помимо собственно установки, схема позволяет бенефициарам приобрести зарядное устройство, преобразовать свою домашнюю электрическую установку с однофазной на трехфазную и купить аккумулятор для хранения энергии, которая будет вырабатываться домашней станцией. Программа имеет обратную силу с 1 февраля этого года и будет действовать до 20 декабря 2023 года или до тех пор, пока все средства не будут израсходованы. Размер субсидии на установку фотоэлектрической станции подзарядки составляет 750 евро за кВт, но не более 1500 евро на одно транспортное средство.

Размеры субсидий

Субсидии на дополнительные расходы распределяются следующим образом:

― покупка и установка зарядного устройства 600 евро,

― перевод домашней электроустановки с однофазной на трехфазную 450 евро,

― покупка/ установка аккумулятора 750 евро за кВт-ч.

Максимальная сумма гранта на одну заявку составляет 2000 евро.

Субсидирование домашних станций подзарядки реализуется в рамках плана восстановления и устойчивости.

Заявки принимаются только онлайн по ссылке.

Обилие свадеб и крещений, перенесенных с 2020 и 2021 годов, большое количество мероприятий в городах и селениях в сочетании со скидками, которые действуют с начала июля, оказывают очень благотворное влияние на отрасль розничной торговли, говорят эксперты.

Несмотря на рост цен, одежду и обувь в июле стали покупать так же, как и до пандемии, восстановился объем продаж. Генеральный секретарь Кипрской ассоциации розничной торговли (ПАСИЛЕ) Мариос Антониу сказал, что июль был очень хорошим месяцем для сектора, и участники рынка ожидают, что август будет таким же. «В отдельных магазинах одежды и обуви, универмагах и торговых центрах ветер перемен дует с июля, когда начались скидки. Люди в этом году почувствовали себя по-настоящему свободными, прислушались к своим желаниям и обновили свой гардероб. Июль стал очень хорошим месяцем с точки зрения туристического потока, особенно в регионе Пафоса», – сказал Антониу.

В супермаркетах покупают меньше

Что касается супермаркетов, то, по его словам, клиенты стали делать покупки по заранее составленному списку, чтобы ограничить непредвиденные расходы, и пытаются «сократить свою корзину покупок, подбирая более экономичные решения». Характерно, например, что за последний месяц увеличились продажи замороженных продуктов.

Преимущества охлажденного воздуха

Владельцы больших торговых центров также выражают полное удовлетворение ситуацией.

«Для торговых центров июль стал очень хорошим месяцем с точки зрения оборота магазинов, которые в них размещены, а также с точки зрения проходимости», ― сказал генеральный директор Nicosia Mall Йоргос Георгиу. За первые семь месяцев 2022 года оборот превысил аналогичные показатели 2019 года на 18,5%. Однако, в отличие от магазинов, кафе и рестораны в торговых центрах не вернулись к прежним объемам продаж. Ожидается, что это изменится в августе, когда большая часть жителей будет на каникулах, так как «моллы» могут предложить всем членам семьи шопинг и развлечения в хорошо охлажденном помещении.

Руководитель отдела коммуникаций и продвижения ТЦ Metropolis Mall в Ларнаке Марилена Палази тоже довольно ситуацией, заявив, что почти во всех магазинах торгового центра товары буквально смели с полок благодаря начавшимся скидкам. «Магазины распродали все свои запасы. Некоторые магазины уже начали выставлять свои зимние товары и продукцию для школьников», – отметила она.

Маленькие магазины закрываются

Популярность торговых центров, однако, не у всех вызывает сочувствие. Генеральный секретарь профсоюза ПОВЕК Стефанос Курсарис рассказал, что из-за того, что конкуренцию с торговым центром выдержать невозможно, в Ларнаке закрывается один магазин за другим. Предприятия в Айя-Напе и Протарасе также сталкиваются с проблемами из-за меньшего, чем раньше, количества туристов. Что касается эффективности скидок, то их смысл потерялся. «Выгодные предложения идут круглый год, поэтому институт скидок пришел в упадок из-за отсутствия институциональной правовой базы и из-за того, что компетентное министерство не осуществляет контроль за тем, что происходит. Феномен непрерывных предложений не помогает ни предпринимателю, ни потребителям, потому что они не знают, совершают ли они покупки по действительно сниженным ценам», – считает Курсарис. С другой стороны удар по малым предприятиям наносят рост цен на энергоносители и высокая арендная плата.

Доходы от туризма превысили 500 млн евро, согласно данным Статистической службы, опубликованным 1 августа. По результатам исследования, проведенного Статистической службой, за период с января по май 2022 года доходы от туризма оцениваются в 543 млн евро.

Напомним, в аналогичный период 2020 года доходы от туризма равнялись 115,3 млн евро, а за первые пять месяцев 2021 года ― 123 млн евро. Что касается мая, то доходы от туризма в этом месяце достигали 221 млн евро, что почти в три раза больше, чем в мае 2021 года (76,7 млн евро). В мае 2019 года доходы от туризма составляли 277,6 млн евро.

В Фамагусте туристов достаточно

Владельцы отелей в регионе Фамагусты довольны количеством туристов, этим летом приехавшим на Кипр. Президент Кипрской ассоциации отельеров (ПАСИКСЕ) в Фамагусте Дорос Таккас сказал Кипрскому агентству новостей, что уровень заполняемости отелей в июле достиг 80%. «Это на данный момент был наш лучший месяц в этом году, хотя мы ожидаем, что в августе этот процент вырастет еще больше, ― сказал Таккас. ― Однако мы не можем делать прогнозы о том, какой будет ситуация после летнего сезона из-за экономической нестабильности в Европе. Нам просто нужно будет подождать и посмотреть, как будет развиваться ситуация. Мы не можем делать прогнозы и строить планы в соответствии со сценариями, которые могут не сбыться». Тем не менее, исходя из тех экономических трудностей, с которыми сталкиваются жители Европы, похоже, что 2023 год станет еще одним трудным годом для индустрии туризма, считает Таккас.

В пять раз больше туристов на Кипре

По данным французского информационного агентства AFP, с января по июнь 2022 года Кипр посетили 1,2 миллиона человек, что почти в пять раз больше, чем в прошлом году. Пока общее число посетителей остается на 25% ниже, чем за аналогичный период 2019 года, когда за первые восемь месяцев на Кипр прибыли 1,63 миллиона туристов. В первой половине этого года британские туристы составили почти 2/5 от общего числа посетителей, за ними следуют израильтяне, на долю которых пришлось 7% прибывших, затем идут Польша, Германия и Греция. «Различные секторы предприняли множество усилий, чтобы привлечь туристов с других рынков, таких как немецкий, польский, итальянский и французский», ― сказал агентству AFP Харис Папахараламбус, представитель Ассоциации кипрских туристических агентов (AКTA).

Последствия кризисов

В статье AFP, которую цитирует издание «Политис», говорится о проблемах, с которыми сталкивается туристическая индустрия Кипра. Сектор, который «принес 2,68 миллиарда евро в 2019 году, то есть составил 15% от ВВП Кипра, все еще подсчитывает стоимость катастрофических пандемийных лет, когда в путешествиях царил хаос». В 2019 году, до начала пандемии, пятую часть туристов составляли россияне (782 000 из 3,9 млн), что делало российский рынок вторым по величине для острова (после Великобритании). В прошлом году, несмотря на строгие ограничения на поездки, этот показатель вырос до 25%, а число прибывших из России составило почти 520 000 человек из 1,93 миллиона. «В этом году мы ожидали 800 000 российских туристов», ― сказал Харис Лоизидис, глава Кипрской ассоциации отельеров. Влияет на туризм и увеличение цен на топливо. Поскольку туристы пользуются кондиционерами, чтобы справиться с жарой, отелям приходится платить «астрономические счета за свет», говорит Лоизидис. «ЕС должен решить эту проблему и помочь бизнесу, особенно в это время, когда бушует инфляция», ― считает он.

Кипр попал в число четырех стран еврозоны с наибольшими расходами на заработную плату в процентах от ВВП. При этом, отмечено, что и по высоким ставкам ипотечного кредитования, Кипр также на одном из первых мест. Об этом говорится в исследовании Европейского Центрального банка (ЕЦБ).

Кипр входит в число четырех стран еврозоны, которые потратили больше всего бюджетных средств на жалования государственным служащим ― более 13% от ВВП. Вместе с Кипром такие же высокие расходы на госслужащих у Греции, Бельгии и Франции. Данные приводятся за 2020 год, но ясно, что и сейчас ситуация не изменилась к лучшему. Наоборот, на Кипре стало больше госслужащих, несмотря на цифровизацию.

Кипр много платит госслужащим

В еврозоне средний уровень затрат на заработную плату госслужащим составил 7,2% от ВВП в 2019 году и 7,8% от ВВП в 2020 году. Государственные расходы на заработную плату и пенсии в еврозоне в последнее время значительно возросли: в прошлом году объем государственных зарплат достиг 922 млрд евро или 7,6% от ВВП (без учета социальных взносов работодателей). Объем государственных пенсий оценивается в 1,484 млрд евро (12,1% от ВВП). Полная или частичная индексация предусмотрена только в пяти странах. На Кипре, как и на Мальте, индексация зарплат госслужащих носит ограниченный характер. Большая часть заработной платы в еврозоне устанавливается в соответствии с коллективными государственными контрактами, охватывающими все или некоторые секторы государственной службы.

Высокие ставки по ипотеке

Другая характерная особенность Кипра, о которой стало известно из отчета ЕЦБ ― одни из самых высоких ставок по ипотечным кредитам в еврозоне. Ставка по ипотеке на Кипре составляет 2,31%, это пятый по величине показатель после Греции (3,07%), Ирландии (2,81%), Германии (2,57%) и Латвии (2,48%). Данные приводятся по состоянию на июнь 2022 года, до повышения ключевой ставки Европейским Центробанком.

Процентные ставки могут сдержать инфляцию?

По сравнению с маем кипрские ипотечные ставки фиксируют небольшой рост на 0,04 процентных пункта, а по сравнению с сентябрем 2021 года ― на 0,12 п.п.

Средняя ставка по ипотечным кредитам в еврозоне в июне составила 1,94%, что на 0,16 пунктов больше, чем в мае. Средние процентные ставки сейчас на 0,64 процентных пункта выше минимума в 1,3%, зафиксированного в сентябре прошлого года. Это самый большой рост стоимости ипотечного кредитования с 2006 года.

По данным издания Financial Times, ставки по ипотечным кредитам в еврозоне резко растут, создавая перспективы замедления роста рынка жилья, поскольку государственная поддержка во время пандемии коронавируса и стремление потребителей приобретать квартиры большей площади привели к повышению цен на жилую нежвижимость. Процентные ставки увеличиваются во всех странах с развитой экономикой, так как центральные банки этих стран настаивают на повышении ставок в попытке контролировать инфляцию.

Согласно данным ЕЦБ, процентные ставки росли быстрее всего в Германии и Италии, наименьший рост был зафиксирован во Франции и Испании. Франция, Португалия и Финляндия имеют самые низкие процентные ставки по ипотеке.

Ожидается, что ипотечные кредиты станут дороже уже в ближайшие месяцы, после решения ЕЦБ повысить ключевую ставку по депозитам. Еще один рост ― примерно на 0,5 пункта ― прогнозируют в сентябре. Инфляция достигла нового максимума в 8,9% за год. Это новый рекордный максимум для еврозоны, который в четыре раза превышает целевой показатель центрального банка в 2%. Банки на фоне этого ожидают снижения спроса на кредиты.

Один из самых важных и наиболее часто задаваемых вопросов при переоформлении объектов недвижимости касается перечня документов, необходимых для предоставления в соответствующие службы. Что не удивительно, учитывая огромное число сделок купли-продажи, дарения и переоформления недвижимости на Кипре. В этой статье из архива* «Успешного бизнеса» предлагаем вам краткий обзор перечня таких документов, необходимых в каждом конкретном случае.

Общим для всех операций перевода права собственности на объект, а также их налогообложения является предоставление заполненной Декларации об отчуждении недвижимого имущества (форма Т.Ф.401), где указываются данные сторон сделок, а также характеристики объекта недвижимости. Данную декларацию должны сопровождать следующие документы (остановимся на наиболее часто осуществляемых сделках).

1. При сделках отчуждения между физическими лицами, не состоящими в родственных связях предоставляются договор купли-продажи (оригинал или заверенная копия); данные или квитанции, подтверждающие стоимость сделки (с учетом того, когда объект недвижимости построен, сдан в эксплуатацию или последний раз продан); справка из банка, если объект недвижимости был приобретен в кредит и кредит на момент отчуждения не погашен; договора комиссии с агентством недвижимости, если таковой имеется; при необходимости – справка об энергопотреблении от Электрической компании Кипра; договор сдачи в аренду объекта недвижимости, если таковой был. Кроме того, если продается объект, выступавший основным местом жительства, и при этом предыдущим собственником был приобретен с применением льготной ставки НДС, нужно предоставить документ, подтверждающий данную операцию;

2. При сделках продажи между юридическими лицами, либо юридическим и физическим лицом предоставляются свидетельства акционеров, выданные Департаментом регистрации и ликвидации компаний; если заинтересованные стороны сделки не являются зависимыми лицами, предоставляются данные о физических лицах, участвующих в сделке; оплаченные счета отчислений на капитал при продаже имущества компанией; проектная документация в случае продажи зависимому лицу или родственнику; а также документы, подтверждающие экономическое состояние субъекта за все годы в случае продажи юридическим лицом;

3. При сделках продажи между физическими лицами, состоящими в родстве (до третьей степени родства) предоставляются все документы, перечисленные в п. 1, а также заключение независимого частного оценщика;

4. При договорах дарения между физическими лицами, состоящими в родстве (до третьей степени родства) предоставляются заполненные формы Ν. 303 и Ν. 313, а также справка об энергопотреблении от Электрической компании Кипра;

5. При договорах дарения семейной компании или от семейной компании ее члену предоставляется заполненная форма Ε.Πρ.117, заверенная копия устава компании и свидетельство акционеров, выданное Департаментом регистрации и ликвидации компаний;

6. При подаче заявления на компенсацию налога на недвижимость со стороны продавцов предоставляются заполненная заявка по форме Τ.Φ.314, копия регистрационного документа собственности, копия договора купли-продажи, чек об уплате налога на недвижимость со стороны продавца, заявление собственника по форме Τ.Φ.303, справка из кадастра Δ.Ε. 246, а также справка от продавца о дате передачи объекта недвижимости покупателю;

7. При освобождении от уплаты налога при реструктуризации кредита при продаже объектов недвижимости, которые являются объектом налогообложения на прирост капитала предоставляются форма Т.Ф.415 в электронном и распечатанном виде, заполненная форма Т.Ф.415В в случае продажи объекта недвижимости третьему лицу; соглашение о реструктуризации кредита; кредитный договор; документ, подтверждающий состояние погашения кредита; заключение кадастра, а также другие документы в зависимости от особенностей реструктуризации.

По любым вопросам перевода права собственности на объект недвижимости можно обращаться по тел. 22 308 191 и 22 308 194; по вопросам, касающимся вступления в права наследства, – по тел. 22 308 195 и 22 308 196.

Более подробную информацию можно найти в директиве 13/2021 Налоговой службы.

Ярослава Дубенюк-Панайотопулу

* Эта статья из архива «Успешного бизнеса» была впервые опубликована в мае 2021 г. Обращаем ваше внимание, что с момента написания текста могли произойти изменения, либо часть информации могла устареть.

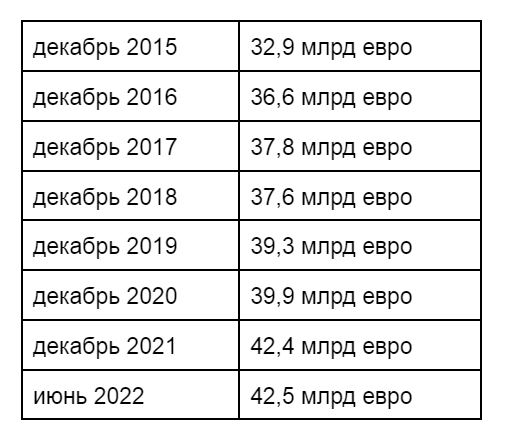

Объемы депозитов жителей Кипра спустя два года после пандемии, на фоне неблагоприятной экономической ситуации в Европе и мире начали увеличиваться. Говорит ли это о доверии к банкам или о том, что киприоты предпочитают отложить «на черный день»?

Как показывают последние данные Центрального банка, в июне 2021 года объемы депозитов жителей Кипра составляли 40,6 млрд евро, а в июне 2022 года – уже 42,5 млрд евро. По сравнению с допандемийным 2019 годом объем депозитов увеличился на 3,2 млрд евро. Для сравнения, через два года после финансового кризиса 2013 года, в декабре 2015, общая сумма депозитов киприотов равнялась 32,9 млрд евро.

Динамика роста объема депозитов видна в следующей таблице:

А в других странах ЕС депозиты растут не так быстро

В то же время, по данным Европейского центрального банка (ЕЦБ), в еврозоне только 20% граждан увеличили свои сбережения во время пандемии. ЕЦБ опубликовал данные исследования за 2020 и 2021 годы, зафиксировав снижение сбережений на 16% из-за пандемии и ее последствий. Согласно результатам опроса, сбережения обычно не делали те, кто получал государственную финансовую поддержку. Эта же категория была склонна к потреблению больше, чем остальные жители.

Как пандемия повлияла на приоритеты?

Что касается поведения потребителей до и после пандемии, то, согласно исследованию ЕЦБ, за 12 месяцев, предшествовавших пандемии, изменения в их потребительском поведении были минимальны. Зато после пандемии 30% респондентов сократили объемы покупок. При этом, 15% опрошенных ответили, что объемы их покупок, наоборот, увеличились. Большинство планирует вернуться к уровням потребления, существовавшим до пандемии.

Кроме того, данные того же опроса показывают, что 20%, которым удалось увеличить свои сбережения, будут более устойчивы к продолжающемуся энергетическому кризису и повышению цен.

30 июня 2021 года закончился переходный период, в течение которого кипрские компании могли использовать в своей работе положения предыдущего режима налогообложения интеллектуальной собственности (ИС). В этой статье мы описываем основные налоговые положения режима защиты ИС и объясняем*, в чем его преимущества для бизнеса.

С 1 июля 2021 г.все без исключения экономические субъекты подпадают под действие обновленной версии режима, применяемой с 2016 года и разработанной в соответствии с нормативной базой ОЭСР для налогообложения ИС компаний, имеющих дело с исследованиями и разработками.

Несмотря на то, что реформа ИС-законодательства изначально была нацелена лишь на приведение кипрского режима налогообложения в соответствие правилам Плана BEPS (5), в итоге она способствовала привлечению на Кипр крупных игроков, что привело к росту рынка и созданию новых рабочих мест.

Следует отметить, что в рамках режима налогообложения ИС на Кипре применяется принцип «модифицированного подхода к взаимосвязи» (Modified Nexus Approach), принятого ОЭСР. Общее связывание расходов с аккумулируемым доходом является основополагающим в применении МПВ.

По сути, налоговое законодательство допускает принятие к вычету 80% «квалифицируемой прибыли», возникающей в результате эксплуатации «квалифицируемого актива ИС», и одновременно, только 20% убытков (в том случае, если формируется убыток, а не прибыль) может быть передано между компаниями группы и/ или зачтено в счет будущей прибыли (максимум пять лет).

Термин «квалифицируемый актив ИС» означает, что актив: приобретается, разрабатывается или эксплуатируется любым лицом в рамках ведения хозяйственной деятельности; представляет собой (i) объект интеллектуальной собственности, не относящийся к маркетингу, и (ii) результат научно-исследовательской деятельности; и включает патенты, компьютерное программное обеспечение и другие нематериальные активы, которые являются неочевидными, полезными и новыми. При этом валовой доход налогоплательщика от использования всех нематериальных активов не должен превышать €7,5 млн в год, а в случае группы – годовой валовой доход группы не должен превышать €50 млн, согласно среднему за пять лет значению в обоих случаях. Квалифицируемые активы ИС не включают торговые марки, в том числе фирменные наименования, права на изображения и другие права интеллектуальной собственности, используемые для маркетинга продуктов или услуг.

«Квалифицируемая прибыль», 80% которой налогоплательщик может принять к вычету, рассчитывается по следующей формуле (коэффициент взаимосвязи):

В связи с квалифицированным активом ИС термин «квалифицируемые расходы» означает расходы на НИОКР, исключительно и полностью связанные с разработкой, усовершенствованием или созданием такого актива; эти расходы понесены в отчетном году и имеют непосредственное отношение к данному активу, а также включают (но не ограничиваются ими) расходы на оплату труда, амортизационные издержки, расходы на НИОКР, выполняемые несвязанными сторонами, и прочие расходы, имеющие прямое отношение к НИОКР. При этом к квалифицируемым расходам не относятся затраты на приобретение, процентные платежи, затраты на строительство, любые расходы на НИОКР, выплаченные связанным сторонам, а также любые издержки, которые не имеют непосредственного отношения к конкретному активу ИС.

Законодательными нормами также допускается дополнение (up-lift) квалифицируемых расходов, понесенных квалифицируемым налогоплательщиком, которое рассчитывается как меньшее из двух: 30% от квалифицируемых расходов или совокупная стоимость приобретения и любых НИОКР, выполненных связанными сторонами, которые имеют отношение к квалифицируемому активу ИС.

Термин «Совокупные расходы» означает квалифицируемые расходы, затраты на приобретение и на работы, выполненные связанными сторонами, которые имеют отношение к квалифицируемому активу ИС в то время, когда они понесены.

«Совокупный доход» означает валовой доход, получаемый от квалифицируемого актива ИС в отчетном году после вычета любых прямых издержек, понесенных целиком и исключительно в целях генерирования такого дохода. Он включает (но не ограничивается ими) роялти и лицензионные платежи, выплаты по ущербу и компенсации, а также любой встроенный ИС-доход от продажи продуктов и использования процессов, непосредственно связанных с активом ИС.

Любые расходы на приобретение или разработку актива ИС, понесенные лицом, которое задействовано в ведении хозяйственной деятельности, при условии, что такие расходы носят капитальный характер, амортизируются на протяжении срока полезного использования данного актива (максимум 20 лет или период, установленный налоговым комиссаром) и представляют собой прямые издержки.

Такие положения, неразрывно связанные с необходимостью видеть реальную значимую деятельность кипрских ИС-компаний (то есть наличие квалифицированного, опытного персонала для формирования расходов на НИОКР), привели к повышению важности Кипра как центра ИС. Многие компании, в основном занимающиеся созданием программного обеспечения, перенесли свои основные департаменты по исследованиям и разработкам на Кипр или наняли для разработки объектов ИС местных специалистов, при этом пользуясь возможностью вычета 80% квалифицируемой прибыли из налогооблагаемой базы. Эти положения также привлекли на Кипр новые отрасли, что положительно сказалось на устойчивом росте экономики в целом.

Джордж Маркидис

Партнер, KPMG

Этот адрес электронной почты защищён от спам-ботов. У вас должен быть включен JavaScript для просмотра.

* Эта статья из архива «Успешного бизнеса» была впервые опубликована в июле 2021 г. Обращаем ваше внимание, что с момента написания текста могли произойти изменения, либо часть информации могла устареть.

Одним из первых шагов при запуске нового бизнеса будет выбор названия будущей компании. Его недостаточно просто придумать – оно должно также получить официальное одобрение Департамента регистрации и ликвидации компаний. Последнее, кстати, касается и тех случаев, когда компания перебазируется на Кипр из-за рубежа и хочет продолжить деятельность под существующим названием. Давайте разберемся*, что для этого нужно.

Во многих случаях самое быстрое и очевидное решение вам предложат ваши юристы: воспользоваться одним из названий, заранее зарегистрированных в Реестре компаний. Это вариант годится, если для вас название бизнеса не принципиально. Если же это не ваш случай, процедура следующая.

Поиск и термины

Определившись с названием, воспользуйтесь онлайн-поиском по реестру. Так вы сможете убедиться, что там нет других компаний с таким же или очень похожим названием.

Чтобы получить одобрение Департамента, название не должно быть слишком похожим на название уже существующей компании, а также не должно быть вводящим в заблуждение или нежелательным.

Например, оно не может:

- указывать на какую-либо связь с Республикой Кипр, ее высшим руководством (президентом, министрами, министерствами) или с правительством иностранного государства, если, конечно, это не отвечает реальному положению дел;

- в общих чертах указывать на тип деятельности, качество или местонахождение;

- использовать английские и греческие слова, обозначающие «национальный», «международный», «Евросоюз», «Европа», «кооперативным», «муниципальный», «признанный» и пр.

- включать имя или фамилию лиц, кроме директора, акционера или владельца;

- содержать специальные символы и знаки препинания: @, €, %, !

Кроме того, отдельно регулируется использование ряда специальных терминов, таких как: «банк», «кредитный союз», «академия», «колледж», «казино», «радио», «телевидение», «страховая компания» и пр. Включение их в название юридического лица требует получения разрешения от соответствующего регулятора, например, Центробанка, Минобразования или Кипрского управления радио и телевидения. То же относится к аббревиатурам LLC (нужно разрешение Юридической службы республики), а также FCIC, AIF, RAIF и т. п. – здесь требуется согласие Кипрской комиссии по ценным бумагам и биржам CySEC.

Если же на Кипре уже существует компания с названием, очень похожим на то, на которое нацелились вы, следует заручиться ее письменным согласием на использование этого названия.

Получив заявку на регистрацию названия, сотрудники Департамента также проверят его, причем в отношении компаний, зарегистрированных не только на Кипре, но и за рубежом. То есть, вы не сможете, к примеру, назвать свою кипрскую фирму Coca Cola. Чтобы избежать накладок, рекомендуется заранее проверить, не является ли выбранное вами название уже зарегистрированной кем-то торговой маркой.

Limited/Ltd

В зависимости от формы собственности компании, ее название должно заканчиваться аббревиатурой:

- LTD/Limited – для частных компаний с ограниченной ответственностью;

- PLC/ Public Company Limited (или варианты: PUBLIC CO. LTD, PUBLIC LTD и пр.) – для открытых акционерных обществ.

Некоммерческим организациям в ряде случае разрешается не использовать Limited в названии.

Подача заявки

Подать заявление в Департамент на регистрацию/смену названия можно как онлайн, так и лично или по почте. Бланки заявления и сопроводительной анкеты можно найти здесь.

К заполненным формам следует приложить:

- при использовании оговоренных выше специализированных терминов – разрешение от соответствующего регулирующего органа или другой компании;

- квитанцию об оплате пошлины в размере €10. Для обработки заявки по ускоренной процедуре следует дополнительно заплатить €20.

Результаты рассмотрения заявления можно узнать онлайн. После одобрения названия у компании есть шесть месяцев на регистрацию юридического лица.

Критерии оценки

Форма заявления:

- все поля в бланке заявления должны быть корректно заполнены (например, название на которое подается заявка, должно быть указано в форме прописными буквами);

- предоставлено согласие со стороны другой компании или соответствующего регулирующего органа на использование данного названия – в тех случаях, когда это применимо (см. выше).

Сопроводительная анкета: здесь также следует убедиться, что все поля заполнены правильно и предоставлена вся нужная информация.

Основные причины отказа

- Предоставление некорректных или неполных данных, из-за чего невозможно принять решение;

- сходство названия с названием компании, уже существующей на Кипре или за рубежом;

- невыполнение ряда требований организациями, от которых требуется разрешение на использование названия;

- название является «нежелательным» согласно ст. 18 закона «О компаниях»;

- название компании лишь в общем указывает на род деятельности или качество или месторасположение и не имеет отличительных признаков;

- название компании вводит в заблуждение (например, когда масштаб деятельности компании ограничен ресурсно или географически, а название подразумевает обратное).

По материалам Департамента регистрации и ликвидации компаний

* Эта статья из архива «Успешного бизнеса» была впервые опубликована в апреле 2021 г. Обращаем ваше внимание, что с момента написания текста могли произойти изменения, либо часть информации могла устареть.