Что волновало деловых людей 500 лет тому назад? Какой тогда была жизнь на острове, находившемся под властью Венеции? Предлагаем вашему вниманию сохранившиеся в архивах личные письма венецианцев.

Последняя королева Кипра Катерина Корнаро отказалась от престола и передала трон венецианскому совету. Так Кипр оказался в составе венецианского государства: на острове более чем на 80 лет утвердились итальянцы. Каким был Кипр в то время? На этот вопрос можно ответить, используя не научные исторические труды, а настоящую личную переписку, которая сохранилась до наших дней.

ЧТО ДЕЛАТЬ С РАБЫНЕЙ?

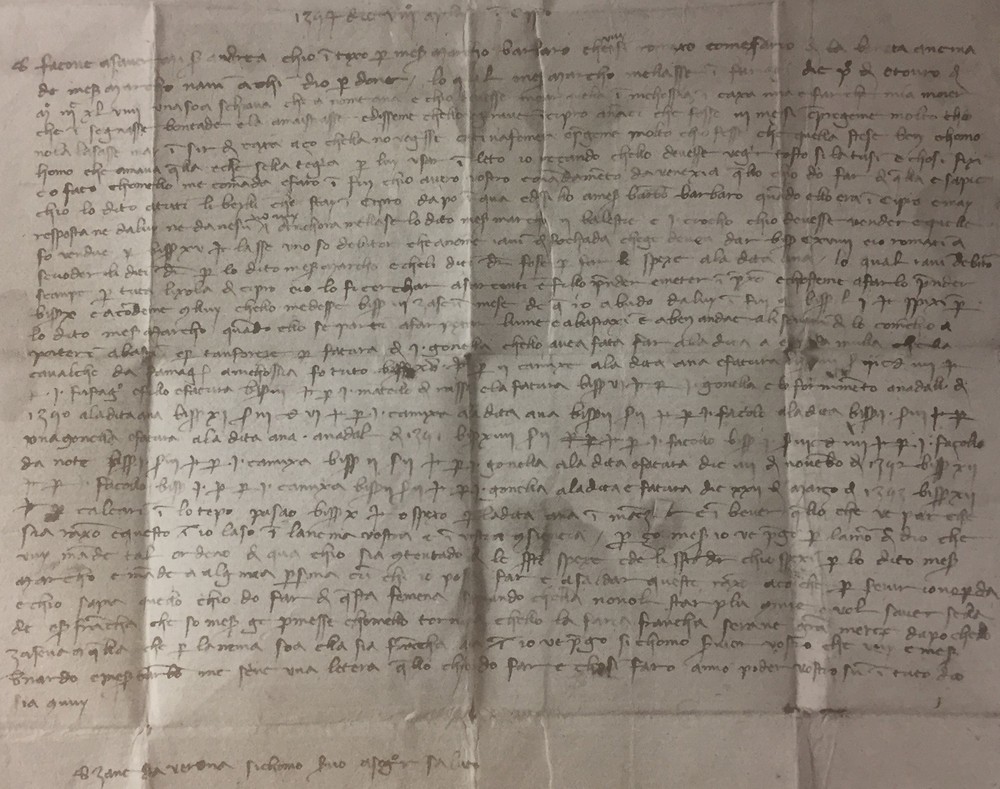

Первое письмо самое необычное. Оно было написано еще в то время, когда Кипр был независимым королевством. Житель Никосии Джованни, уроженец Вероны, писал видному венецианскому политику Андреа Контарини, который был судебным исполнителем по имуществу покойного купца Марко Нани.

Оригинальное письмо / Paul and Nina Pastides Collection

«Данным письмом сообщаю Вам, миссер Андреа, что я узнал от мессера Марко Барбаро о Вашем назначении на должность государственного исполнителя по делу покойного мессера Марко Нани, да простит его Бог. Марко Нани оставил мне 1 октября 1349 года в Фамагусте под присмотр девочку-рабыню Анну и попросил принять ее в свой дом в Никосии, дабы моя жена научила ее ведению хозяйства и добрым манерам. Он сообщил мне, что вернется на Кипр не позже чем через три месяца, и умолял не выпускать девочку из дома, чтобы она не выросла в своенравную женщину. Нежно относясь к ней и держа ее как постельную спутницу, Марко упорно просил меня хорошо о ней заботиться. Полагая, что он вернется быстро, я забрал Анну и забочусь о ней согласно всем его наставлениям до сих пор [т. е. уже почти 5 лет]… Прошу помочь рассчитаться с долгами Марко Нани за заботу о девушке и дать знать, что делать с Анной. Она не хочет оставаться в моем доме, так как Марко Нани обещал ей свободу после своего возвращения. Во имя его светлой памяти, это было бы настоящим актом милосердия, если бы она была отпущена».

Отправлено из Никосии 8 апреля 1354 года, получено в Венеции 14 июня 1354 года.

Судьба бедной Анны нам неизвестна. Из данного письма очевидно, что на Кипре в то время сохранялись пережитки рабства. Подобная ситуация была и в самой Венеции, и во многих других

городах Европы.

ДЕСЯТЬ САХАРНЫХ ГОЛОВОК

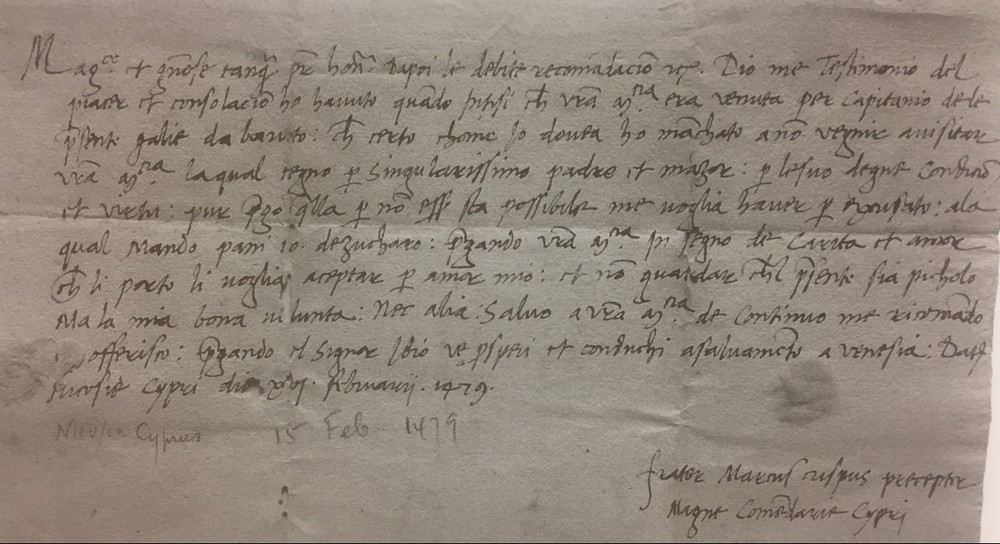

Венецианцы использовали Кипр как перевалочный пункт между Ближним Востоком и Европой. Большинство западноевропейских киприотов были военными или торговцами. Вот пример типичного письма одного венецианского военного, служащего на Кипре, другому. Автор изящно, по этикету того времени, извиняется перед своим знакомым за то, что не смог его посетить на Родосе.

Оригинальное письмо / Paul and Nina Pastides Collection

«Великолепный и великодушный, почитаемый как отец! После стольких рекомендаций, да будет Бог свидетелем, какое удовольствие и утешение я испытал, услышав, что Ваше Величие было назначено капитаном бейрутских галер. Я не смог навестить Ваше Величие, как мне, несомненно, следовало бы, поскольку я вижу в Вас своего отца и старшего, особенно учитывая Вашу достойность и добродетель. Будучи неспособным навестить Вас, я прошу прощения, посылая вам десять сахарных головок в знак моей доброжелательности и любви. Подарок я прошу принять как знак моих чувств. Пожалуйста, не принимайте близко к сердцу этот подарок как дешевый откуп, ведь главное – мое доброе намерение. Мне больше нечего добавить, кроме как рекомендовать и постоянно предлагать себя Вашему Величеству. Да пребудет с Вами Бог и безопасно проводит Вас в Венецию».

Отправлено из Никосии 16 февраля 1479 года. Получено на Родосе 5 марта 1480 года.

В то время Кипром формально всё еще управляла королева Катерина, однако по факту остров уже переходил в руки венецианцев.

ВОЗМОЖНО, БОГ ПРИНЕСЕТ УДАЧУ ВАШЕЙ ИКРЕ

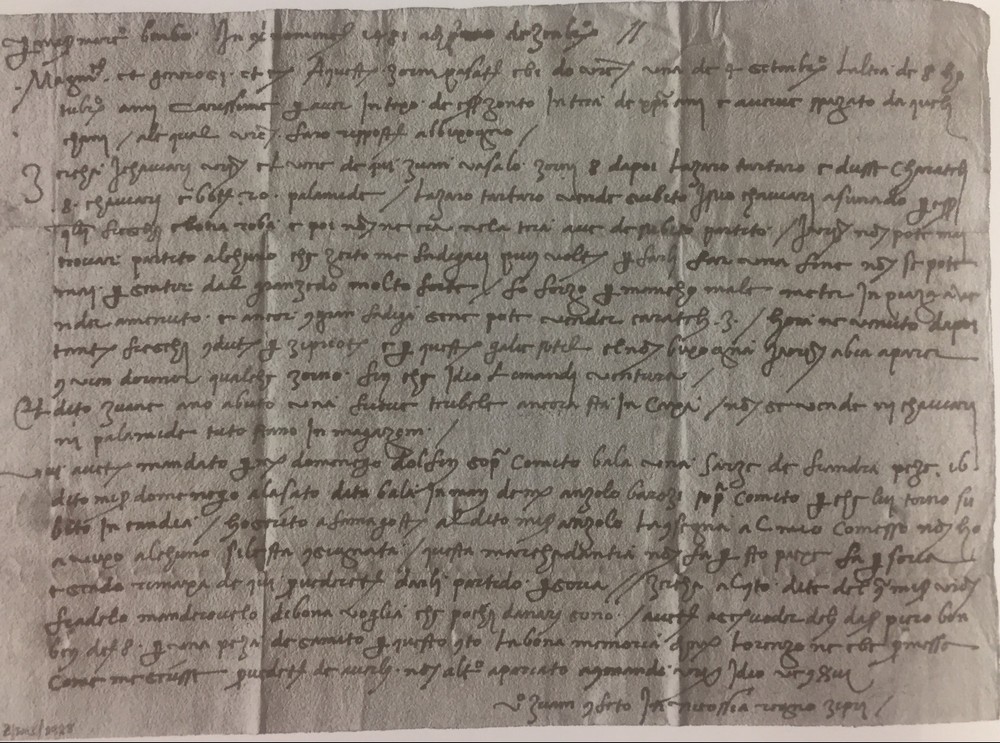

Некоторые венецианцы-киприоты занимались торговлей на острове, например мессер Марко Бамбо.

Оригинальное письмо / Leventis Municipal Museum

«Для мессера Марко Бамбо, во имя Христа, 1 декабря 1481 года. В последние дни я получил два Ваших письма, одно – от 4 сентября, а другое – от 8 октября. Из писем я узнал о том, что Вы вернулись в земли христиан, покинув этих собак. Я отвечу на Ваши вышеупомянутые письма, как и положено. Относительно Вашей икры: Джванни Васало прибыл сюда через 8 дней после Лазаро Тартаро, принеся 8 бочек икры и 20 бочек паламиды. Лазаро Тартаро успел продать свою икру оптом, потому что она была свежей и хорошего качества, а также потому, что в городе икры не хватало, так что он сразу же нашел клиентов. Ваша икра не смогла найти клиентов, хотя я, конечно, несколько раз пытался продать ее, но мне так и не удалось, ибо она имела тухлый запах. Чтобы получить хоть какие-то деньги, я был вынужден поставить бочки на площади для розничной продажи, и даже там мне удалось продать только 3 кеги. Теперь эти киприоты на легких галерах привезли много свежей икры, поэтому я спрятал Вашу на несколько дней, потом, быть может, Бог принесет ей удачу…»

Если с икрой все понятно, то что такое паламида? Это греческое наименование атлантической бониты, популярной рыбы. Примечательно, что паламида и икра добывались в Черном море и оттуда транспортировались на Кипр. Рыбу, естественно, перед отправкой солили.

БОЛЕЗНИ КАК ОСНОВНАЯ ТЕМА

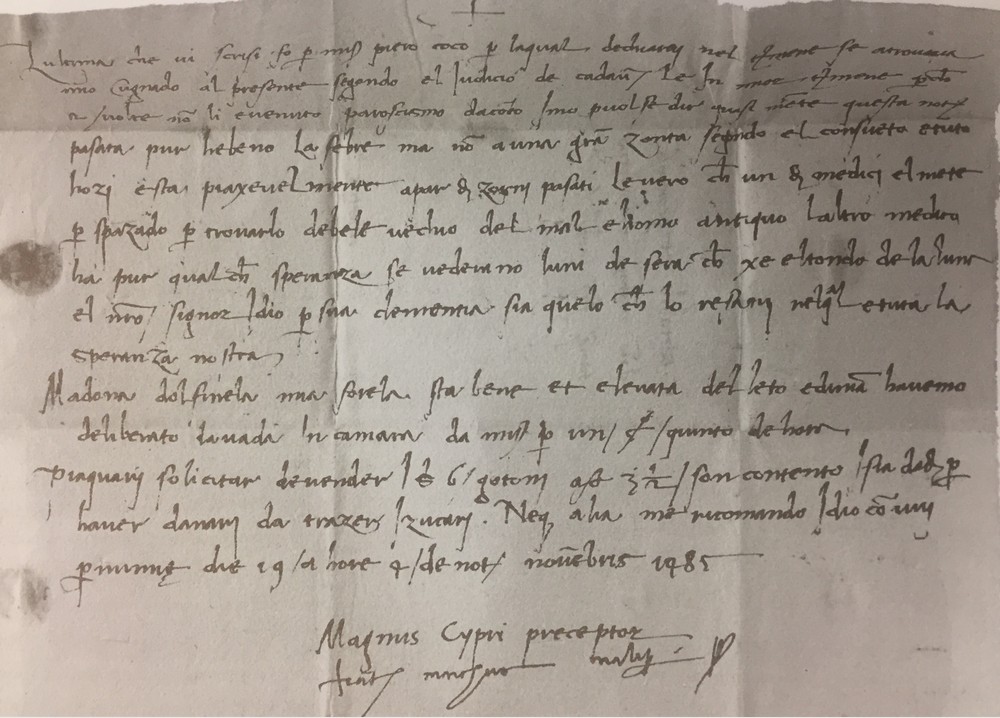

Ну и, наконец, западноевропейские жители Кипра постоянно сообщали друг другу о состоянии здоровья близких людей. Ведь мы сейчас даже представить не можем, какой тогда была медицина. Это письмо написано Марко Малипиеро, главой ордена госпитальеров на Кипре.

Оригинальное письмо / British Columbia Conservation Foundation

«В последнем письме, которое я отправил вам через мессера Пиетро Кокко, я сообщил о здоровье моего шурина. В настоящее время, по общему мнению, его состояние улучшилось, поскольку в последнее время он не страдает ни от сильного пароксизма, ни от чего-либо еще. Прошлой ночью у него была небольшая температура, но не было никаких серьезных приступов, сегодня он чувствует себя хорошо по сравнению с предыдущими днями. По правде говоря, один из врачей считает, что у него нет шансов на выздоровление, потому что он слаб, истощен своей болезнью и очень преклонного возраста. Но у другого доктора есть надежда. Посмотрим, что произойдет к вечеру понедельника под полной луной. Бог наш Господь, по его милости будет тем, кто восстановит его здоровье. Вся наша надежда в Нём. Леди Долфинела, моя сестра, уже здорова и встала с постели, и мы решили позволить ей завтра прийти в комнату мессера на третью часть часа [т. е. на 20 минут]. Пожалуйста, не спешите продавать шесть хлопковых мешков за 3½ дуката. Я согласен с тем, что их следует использовать для вывоза сахара из таможни. Других новостей нет. Бог с тобой».

Почти половина всей переписки, дошедшей до наших дней, содержит описание болезней, от которых страдал либо сам автор, либо его близкие.

Антон КОСТИЧЕВ