Декларации можно подать позже назначенного срока. Льготная ставка предусмотрена, но не для всех. Внесенные в СИДН изменения коснутся только процентов и дивидендов.

26 января 2022 г. “Налоговое управление Кипра” сообщило о продлении сроков для подачи деклараций о взносах на нужды обороны (Special Defence Contribution) и взносах в “Национальную систему здравоохранения” (General Healthcare System). Декларации необходимо предоставить до 31 марта 2022 г. В уведомлении сообщается, что декларация для предполагаемого распределения дивидендов (форма TD 623) была заменена.

Напомним, что согласно изменениям “Соглашения об избежании двойного налогообложения” (СИДН) между Россией и Кипром, выплачиваемые из России дивиденды и проценты по займам будут облагаться налогом по ставке 15%. Предусмотрена льготная ставка, но она будет доступна для ограниченного круга резидентов (фонды и страховые компании). Внесенные в СИДН изменения касаются только дивидендов и процентов. Налогообложение других видов доходов не изменилось. Такие же изменения коснулись и СИДН России с Мальтой. Нидерланды отказались внести поправки в “Соглашение”.

По материалам mov.gov.cy

Living a nomadic lifestyle became a trend in recent years. Paradoxically, the global pandemic helped promote the concept. Last two years proved that many of us could perform our job remotely with the help of technology.

More and more people want to be location independent – either while working remotely for an employer or by setting up their own business activity.

However, the nomadic lifestyle can bring up issues with a residency status, specifically with tax residency. Many travellers do not necessarily think about this in the first place and sometimes totally ignore their tax situation. Even if one decides to do a Tour Around the World, they should think in advance – where and how to declare the revenue. For some, this will be a country where they eventually return to. But those who do not have a permanent home and do not necessarily want to have one, should be very cautious about their tax residency strategy. Similarly, the same applies to the travelling entrepreneurs; they need to make sure that the residency of their business is well-established.

Fortunately, more and more digital nomads are aware of the problems that may arise due to the changes of location and prefer to carefully choose one country as a base and set up the tax residency there.

Digital nomads are privileged since they have the luxury to choose their tax residency country and legally save on taxes. At the same time, many locationindependent expats realised that they don’t have to be on a constant tour to benefit from а nomadic lifestyle. The concept of slow travelling becomes even more popular when we are facing travelling restrictions.

CYPRUS BENEFITS

For any type of nomads – those ‘on the go’ or those who prefer to stay in a place for longer – Cyprus is the ideal place to be.

Most importantly, in 2017, the government introduced very attractive residency rules – one of the best in the world. One can become a Cyprus tax resident when staying in the territory of Cyprus for at least 60 days in a tax year.

The 60-days rule can be used under the condition that this person does not spend more than a sum of 183 days in any other jurisdiction within a tax year and is not a resident (for tax purposes) of another jurisdiction within the same tax year.

A personal tax residency in Cyprus can be favourably combined with a business incorporation on the island since one of the conditions to acquire the residency permit is to be employed or to carry on a business.

Tax residents in Cyprus are taxed on their worldwide income; however, certain exceptions apply. A Cyprus tax resident but non-domiciled in Cyprus is exempt from taxation on his worldwide dividend and ‘passive’ interest income. When becoming a tax resident of Cyprus, the expats can benefit from no taxation of dividends and interest for non-domiciled tax residents – for 17 years of the residency (exemption from Special Defence Contribution which is a local withholding tax on passive income for domiciled tax residents).

Overall, Cyprus is a great jurisdiction to run a business and is often chosen by entrepreneurs for company structuring and tax planning. There are no capital gains tax on sale of securities (selling shares, stocks, various financial instruments) and no withholding tax on dividends, interests, and royalties. Even after the planned increase of the corporate tax rate to 15%, Cyprus will be still one of the most competitive countries to incorporate a company.

Cyprus offers one of the most favourable Intellectual Property systems. The IP regime, also known as the Patent Box or the Innovation Box, introduced in many countries to stimulate research and development (R&D) activities, results in lower taxes, by taxing profits derived from a licence, sublicence, sale, or transfer of eligible IP assets. Under the regime, 80% of the profit earned from the use of intangible assets can be deducted for tax purposes.

The VAT rate is 19% in the case of services rendered to entities in Cyprus or B2C. There is no VAT for the provision of services to entities located outside the EU and when selling B2B services between companies registered for VAT in the EU.

To continue with benefits of becoming a tax resident in Cyprus, we need to mention the 0% rate of the Personal Income Tax for income below €19,500 per year (once reached, it becomes 20-35% depending on the level of income).

Another great incentive is the expatriate tax relief for employment in Cyprus, which is supposed to be extended every five years. In practice, it is granting the application of the 20% or €8,550 (whichever is the lower) tax exemption on remuneration from employment which is exercised in Cyprus by an individual who was resident outside the Republic in the tax year prior to the commencement of his employment on the island.

For instance, under the current framework, as of January 1st, 2020, an individual whose employment in the Republic commences up to the year 2025, has the right to claim the relevant tax exemption for a period of five years (i.e. up to the year 2030 inclusive).

WHAT FUTURE BRINGS

When thinking of Cyprus, we should also appreciate the high-potential dynamic growing economy and investment opportunities. Recently the government decided to promote these qualities and to open for foreign capital.

Cyprus aims to welcome more expats, but not only from the EU, which is a gesture towards the Russian community.

Without a doubt, the current system provides the ease of residency permissions primarily to citizens of the EU countries. The expats from outside the EU zone usually struggle with legalising their residency.

The government introduced the socalled ‘Action Plan’ which will facilitate hiring of employees and offer tax incentives. Some of the proposals will be implemented as from January 2022, however tax relief and new rules for naturalisation will first need relevant legislation. The package is addressed to expats in general, but primary to all foreign companies operating in Cyprus or wishing to establish presence in the country, as well as for Cyprus companies in specific domains related to hi-tech/innovation, research and development, biogenetics and biotechnology, and shipping.

WHAT ABOUT CRYPTOS?

The Action Plan is a very good initiative and will certainly attract more foreign business.

It is a shame though, that the matter of cryptocurrency – being a current global issue and directly connected to digitalisation, is not even mentioned in the Action Plan. In Cyprus we are still waiting for a relevant legislation. The Tax Office in Cyprus is not willing to issue any guidance or interpretations in this matter. For now, since every Cyprus company needs to submit its financial statements, the role of auditors in qualification of such profits is significant.

This means that the interim taxwise solution for now would be keeping the cryptocurrency in a separate entity, like a company. In the current situation, the taxation of profits from cryptos on a corporate level seems to be a less risky option than declaring crypto profits as a physical person.

The only body that recently referred to the subject was the Cyprus Securities and Exchange Commission – when updating its policy of regulation of cryptoassets.

The CySEC document defined specific requirements for companies that seek to be included in the official register of service providers related to cryptocurrencies. At the same time, it describes cryptoassets, but… only those that are regulated… which, of course, is not the case yet. Depending on their structure, cryptoassets can be qualified as financial instruments. Also, without being an official means of payment, they can qualify as ‘electronic money’. Time will show how tax authorities in Cyprus will classify it.

Cyprus is an attractive destination for both business and individuals. Compared to other EU countries, it offers a unique work-life balance blended with a high-quality Mediterranean lifestyle.

In recent years Cyprus has become an international business centre, where many expats found their place to live and digital nomads a great base to stay. With such great potential, it seems to be on the right course for the next decades.

Jowita Jablonska

Founder of CDX Trust – Nomads Club

Этот адрес электронной почты защищён от спам-ботов. У вас должен быть включен JavaScript для просмотра.

CYPRUS ’ACTION PLAN’ HIGHLIGHTS

New policy for employing non-EU country nationals

Issuing of temporary residence and employment permits in Cyprus for high-skilled third-country employees, with a minimum gross monthly salary of €2,500, while a university degree, title, equivalent qualifications, or certificates of relevant experience are also needed.

Family reunification of third-country nationals

Family members of non-EU employees, who are employed under the new residence permit provisions, will also have immediate and free access to Cyprus labour market.

Digital nomad visas

Initially, with a limit of 100 beneficiaries. Digital Nomad Visa is for third-country nationals who wish to live in Cyprus but work remotely for companies operating abroad. The visa will be granted for a period of 12 months, with the right to renew it for another two years. The amount of sufficient resources is set at €3,500 per month.

Application for Cypriot citizenship

Right to submit an application for naturalisation after 5 years of residence and work in the Republic of Cyprus (instead of 7), or after 4 years if they have a recognised certificate of very good knowledge of the Greek language.

Business Facilitation

In areas of hi-tech/innovation, research and development, shipping, biogenetics and biotechnology. Ease of establishing and administering companies shall be improved (company registration, name approval, registration to social insurance, registration to VAT).

Extensions of expatriate reliefs

• Current expat employees will be able to extend the benefit to 17 years.

• Income tax exemption of 50% to new residentsemployees with income between €55,000 and €100,000 for the remaining period of 17 years.

These tax incentives also apply to Cypriots who have lived abroad for at least ten years and wish to repatriate to the Republic.

One could say that this proposal seems to be a little excessive. According to the Plan, tax exemptions addressed to foreign high skilled employees in Cyprus is to be extended for a period of 17 years. It is the same period as current benefit for non-domiciled tax residents. When it makes sense to establish such long period for incentives related to domiciliation, it is not so common to introduce such extensive relief related to the employment. For this reason, we can never take for granted that such benefit would stay within the system for longer.

Tax incentives for R&D expenses and for innovative investments

• Granting an increased discount on research and development expenses (e.g. by 20%)

• Possibility of extending the tax exemption to 50% for investment in certified innovative companies and by corporate investors.

The advancements of blockchain are still young and have the potential to be revolutionary in the future. In few words, blockchain is a combination of three leading technologies:

1. Cryptographic keys

2. A peer-to-peer network containing a shared ledger

3. A means of computing, to store the transactions and records of the network.

Cryptography keys consist of two keys – Private key and Public key. These keys help in performing successful transactions between two parties. Each individual has these two keys, which they use to produce a secure digital identity reference. This secured identity is the most important aspect of blockchain technology. In the world of cryptocurrency, this identity is referred to as ‘digital signature’ and is used for authorising and controlling transactions.

The digital signature is merged with the peer-to-peer network; a large number of individuals who act as authorities use the digital signature to reach a consensus on transactions, among other issues. When they authorise a deal, it is certified by a mathematical verification, which results in a successful secured transaction between the two networkconnected parties. To sum it up, blockchain users employ cryptography keys to perform different types of digital interactions over the peer-to-peer network.

PRIVATE BLOCKCHAIN NETWORKS

Private blockchains operate on closed networks, and tend to work well for private businesses and organisations.

Companies can use private blockchains to customise their accessibility and authorisation preferences, parameters to the network, and other important security options. Only one authority manages a private blockchain network.

PUBLIC BLOCKCHAIN NETWORKS

Bitcoin and other cryptocurrencies originated from public blockchains, which also played a role in popularising DLT. Public blockchains also help eliminate certain challenges and issues, such as security flaws and centralisation.

With DLT, data is distributed across a peer-to-peer network rather than being stored in a single location. A consensus algorithm is used for verifying information authenticity; proof of stake (PoS) and proof of work (PoW) are two frequently used consensus methods.

PERMISSIONED BLOCKCHAIN NETWORKS

Also sometimes known as hybrid blockchains, permissioned blockchain networks are private blockchains that allow special access for authorised individuals. Organisations typically set up these types of blockchains to get the best of both worlds, and it enables better structure when assigning who can participate in the network and in what transactions.

The Cyprus Securities and Exchange Commission (CySEC) has published a clarification on the anti-money laundering and counter-terrorist financing (AML/CFT) supervision for cryptoasset operations undertaken in or from Cyprus. The Successful Business Magazine presents the summary of this publication.

REGISTER OR SUBMIT NOTIFICATION?

If you are a Crypto Asset Services Provider (CASP), within the meaning of the Prevention and Suppression of Money Laundering and Terrorist Financing Law (AML/CFT Law), that provides services in or from Cyprus, you must formally register with CySEC.

If you are a CASP established in the EEA and registered with one or more EEA National Competent Authorities for AML/CFT purposes in relation to all services or activities undertaken or intended to be undertaken in Cyprus (i.e. involving Cypriot residents, including incorporated or unincorporated entities based in Cyprus), you must submit a notification. You should provide evidence in relation to your valid registration for each service or activity.

Where these services or activities are not covered by the framework that governs your registration for AML/CFT purposes, you should submit an application to be registered as a CASP with CySEC.

REGISTER BEFORE STARTING BUSINESS

New businesses must register with CySEC before commencing their operations in or from Cyprus. Existing businesses that demonstrate a material existing crypto-asset activity had to submit an application before the end of October 2021 and be fully compliant with the AML/CFT Law and the Directives issued pursuant to the AML/CFT Law.

REGULATORY FRAMEWORK

The applicable regulatory framework comprises:

• The AML/CFT Law • The CySEC Directive for the CASP register

• The CySEC directive for the prevention and suppression of money laundering and terrorist financing. The regulatory framework includes rules, inter alia, in relation to:

• The fitness and probity of the CASP beneficiaries and persons holding a management

position

• The conditions in relation to CASPs registration

• The organisational and operational requirements

• Preforming Know Your Client and other client due diligence measures

• Drawing the economic profile of clients

• Identifying the source of client funds

• Monitoring the clients’ transactions

• Identifying and reporting suspicious transactions

• Undertaking a comprehensive risk assessment in relation to clients’ activities and take proportionate measures per client, activity and crypto-asset in question.

CySEC’s approach on CASPs and their operations is further elaborated in the Policy Statement PS-01-2021.

HOW TO REGISTER

CASPs that provide services in or from Cyprus must submit a duly completed application form, along with relevant questionnaires and any additional information and/or required evidence, in accordance with CySEC’s Announcements on the submission of applications and relevant correspondence, as amended from time to time and pay the corresponding fee. In addition to this, an electronic version of the application form (i.e. only Form 188-01) should be also submitted at Этот адрес электронной почты защищён от спам-ботов. У вас должен быть включен JavaScript для просмотра.

CASPs established in the EEA that are registered with one or more EEA National Competent Authorities for AML/CFT purposes in relation to all services or activities undertaken or intended to be undertaken in Cyprus, must submit a notification form at Этот адрес электронной почты защищён от спам-ботов. У вас должен быть включен JavaScript для просмотра.

REGISTRATION FEES

CySEC registration charges are as follows:

• €10,000 for the examination of an application. Successful applicants will not be required to pay an additional fee for the first year of their registration.

• €5,000 for the purposes of renewal of registration per year.

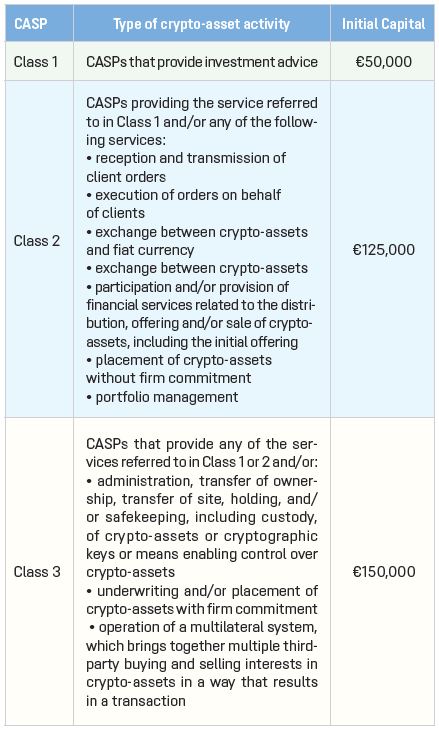

CRYPTO-ASSET ACTIVITIES AND INITIAL CAPITAL

The emerging crypto industry is still unchartered waters in many regards. But the Cyprus Securities and Exchange Commission is working towards eliminating the regulatory gaps and ensure the highest level of investor protection. The Successful Business Magazine asks the Commission head, Dr George Theocharides, about the current crypto landscape in the EU and in Cyprus and the recent and forthcoming regulatory developments.

The emerging crypto industry is still unchartered waters in many regards. But the Cyprus Securities and Exchange Commission is working towards eliminating the regulatory gaps and ensure the highest level of investor protection. The Successful Business Magazine asks the Commission head, Dr George Theocharides, about the current crypto landscape in the EU and in Cyprus and the recent and forthcoming regulatory developments.

In your opinion, what are the greatest regulatory risks that Cyprus faces today?

The trends that we have seen in the last decade or so in financial services are more digitalisation, more online, and mobile trading platforms. We have also seen more sophisticated technologies, such as artificial intelligence, algorithmic trading, blockchain technologies, machine learning, Big Data Analytics, Robo-Advisors, and social trading.

Obviously, these global trends bring many opportunities, but at the same time, they come with risks relating to the protection of the investors, to cases of money laundering and terrorist financing, and risks around cybersecurity.

As regulators, we need to be proactive in understanding these new technologies and how they impact financial services in order to mitigate the risks and protect investors. It is essential that investors understand these risks before proceeding with any investment, so they are not lured into unsuitable investments based on inaccurate or incomplete information. Inconsistent liquidity, unregulated price discovery mechanisms, insider dealing and market abuse in relation to crypto-assets, lack of pre- and post- trade transparency rules, all undermine investor protection. The nature of cryptoassets, which means they are to some extent anonymous or pseudo-anonymous and can be used in the context of electronic contactless transactions and from anonymous crypto wallets and other emerging products, also makes them vulnerable to the risk of money laundering and the financing of terrorism.

What's the solution then?

When it comes to digital assets andWhen it comes to digital assets andcryptoassets, the regulation is evolving. There is a lot of work being done both atThere is a lot of work being done both atthe national and European level. A fewmonths ago, the Cyprus Securities andExchange Commission (CySEC) issueda Policy Statement on the Registrationand Operations of Crypto Asset ServicesProviders (CASP) to outline its finalisedrules for CASPs under the AML/CFTLaw. Additionally, we issued the CASPRegistration Directive and the Directivefor the Prevention and Suppressionof Money Laundering and TerroristFinancing, which elaborates on the nextsteps for CASPs and CySEC’s expectations.We expect Crypto Asset ServicesProviders to abide by their obligationsstemming from CASP Rules, includingbut not limited to their obligationsamong others on:

- the fitness and probity of the CASPBeneficiaries and persons holding a management position

- performing Know Your Client and other client due diligence measures

- drawing the economic profile and identifying the source of funds of their clients

- identifying and reporting suspicious transactions, and

- undertaking a comprehensive risk assessment in relation to their clients and activities and take proportionate measures per client, activity and cryptoasset in question.

Details can be found on the CySECDetails can be found on the CySECwebsite, www.cysec.gov.cy.

CySECalso continues to analyse market practicesand will assess the effectiveness ofexisting rules. Where necessary, we willact to issue further guidance to ensurethe compliance of supervised entitieswith the regulatory framework. CySECexpects these kinds of initiatives toalleviate some, but not all, of the risksinvolved in cryptoasset space, and wewelcome developments at EU level,under the proposed Regulation on Marketsin Crypto Assets (MiCA).

In September 2020, the EuropeanCommission proposed a new regulationon cryptoassets (MiCA). This regulationwill form part of the EU’s Digital FinanceStrategy and is expected to significantlyimpact the operation of the crypto marketin the EU. It will increase consumerprotection by establishing clear cryptoindustry conduct and introduce newlicencing requirements. This proposal,which covers cryptoassets falling outsideexisting EU financial services legislation,as well as e-money tokens, has four generaland related objectives.

The first objective is one of legalcertainty. For cryptoasset markets todevelop within the EU, there is a needfor a sound legal framework, clearlydefining the regulatory treatment ofall cryptoassets that are not covered byexisting financial services legislation.The second objective is to support innovation.The development of cryptoassetsand the wider use of DLT requires a safeand proportionate framework to supportinnovation and fair competition. Thethird objective is to instil appropriatelevels of consumer and investor protectionand market integrity given thatcryptoassets not covered by existingfinancial services legislation presentmany of the same risks as more familiarfinancial instruments. Finally, thefourth objective is to ensure financial stability.

Cyprus has attracted a numberCyprus has attracted a numberof large CIF companies and someconcentrate in CFDs. These tendto have hundreds of thousands oftrading accounts and millions oftransactions every day. Are youconfident that Cyprus' currentregulatory system is adequate toprotect investor interests in companieslike this?

EU financial regulation applies uniformlyto all EU Member States, savefor certain minor Member State discretionsprovided for in the respective EUlegislation. As a result, investment firmsdomiciled in any of the EU MemberStates must abide to the same rulesand in return, benefit from the right tofreely provide their services throughoutthe EU. The regulatory and supervisorylandscape of the financial sector inCyprus mirrors that of the rest of the EUso that investors benefit from the highstandards of protection we enforce.

I should also mention that – untilI should also mention that – untilMiCA becomes effective – a nationalBill has been drafted by the Ministry ofFinance (an Umbrella Law) to regulate the development of DLT-Blockchainthe development of DLT-BlockchainTechnology/Smart Contracts and providelegal certainty to this market.Under this Bill, CySEC is empowered todraft other legislative amendments if itdeems necessary for further regulatingthe provision of investment services inthis space.

Clearly, there is a high level of demandClearly, there is a high level of demandglobally for these products. CySEC hasalways held the belief that regulatingthese products appropriately is the safest,most diligent way of allowing thesefirms to provide these services, and ismost in line with serving investors’ interests.We continually assess and monitorregulated entities to tackle any concerningpractices to ensure that investorsprotection is not compromised. Since2015, CySEC applies a risk-based supervisoryapproach, which governs howwe determine the entities and marketsegments that pose the greatest risks toinvestors, and which are subject to theclosest scrutiny.

Our risk-based supervisory approachfollows the same blueprint for supervisionof other European supervisors andwe have been in constant and close collaborationwith ESMA and IOSCO.

According to our annual SupervisoryAction Plans, each year both onsiteinspections and desk-top reviewsare undertaken on supervised entities,together with full audit inspections orthematic or targeted basis. As a result,CySEC imposed more than €10 millionadministrative fines only for CIFs. Italso suspended the licence of more than30 CIFs, which had significant problemsand called upon them to take a numberof corrective measures to improve theirinternal procedures, regulations andpractices in order to fully comply withtheir legal obligations. In addition, CySECrevoked the operating licence of morethan 15 CIFs, in which serious violationsof the legislation were identified and asignificant number of CIFs voluntarilyresigned from the licence they held.CySEC will continue to conduct in-depthaudits and take all the appropriate actionsto safeguard investor protection and thesmooth functioning of the market.

Also, we are in the process of developingAlso, we are in the process of developingnew procedures and a methodologyto conduct data-driven supervision,which will allow us to identify anyirregularities and risks in the market atan early stage. In this respect, CySEC isresponding to the need to manage BigData with RegTech systems that willuse Artificial Intelligence and CloudComputing. These solutions will enableCySEC to quickly screen data, representinglarge and varied trading volumes,in order to automatically detect risksand irregularities at an earlier stageand, thus, be able to react more quicklyagainst these risks.

A recent CySEC Policy StatementA recent CySEC Policy Statementessentially required investmentservices to be ring-fencedfrom crypto-asset activities. Whatis the rationale underpinning thisapproach?

There is very straight-forward reasonfor this – we don’t want to see issues spillover into investment services from otheractivities such as cryptoasset activitiesthat are not fully regulated.

Do investors in Cyprus understandthe risks of investing in cryptocurrencies? Is CySEC educatinginvestors about these risks?

Right now, what we are seeing aroundthe globe is a lot of hype around cryptoassets;I would even call it irrationalexuberance. This is understandablebecause in the financial markets a newproduct creates a lot of attention similarto the dot.com bubble in the late 1990sor the complex, securitised financialproducts in the 2000s. But I think themarket still has a lot of informationto digest and understand, particularlyin terms of what cryptocurrencies are,how the mechanics of cryptocurrency work, what their purpose is and whatwork, what their purpose is and whatthe risks are.

There is a general lack of knowledgeThere is a general lack of knowledgeamong investors around the globe interms of cryptoassets. Providing knowledgeand education around cryptoassetsand improving financial educationand skills in general is part of the role ofthe regulators. CySEC undertakes variouseducative actions and initiatives,through publications on its websiteand in the media. CySEC participatesin World Investor Week 2021, with theaim of contributing to the global driveto educate and protect investors. Overthe past year, CySEC has been part ofa national effort and is participating atthe ad-hoc Committee for Financial Literacyand Investor Education, togetherwith the Central Bank of Cyprus, theMinistries of Education and Financeand our two state universities to createa national strategy for financial literacy.The aim is to submit the national strategyto the Council of Ministers in early2022. But while education is part of ourmandate, it’s also the responsibility ofmarket participants and the professionalsof the industry to educate investorsabout these types of assets by providingthem with the necessary information inorder to understand if the assets matchtheir needs.

What can investors do to identify/What can investors do to identify/avoid crypto and CFD fraudand scams?

The most important thing investorsmust do when considering an investmentis to do some research into thecompany offering the product or service,and consider whether seeking independentprofessional advice from anotherregulated entity might be appropriate.CySEC has a full list of all the companiesit regulates on its website, which iseasy to check. If a company is not listedby CySEC or another EU competentauthority and is fraudulently claimingto be a licensed firm, investors will nothave the same protections they wouldhave had with a regulated entity. It iscritical that investment firms classifytheir clients in an appropriate mannerso that more sophisticated, and oftenhigher-risk products and services areonly targeted at professional investors.This marketing process must be fair andnot misleading.

CySEC regularly updates its ‘Warnings’website on prevalent scamsand nefarious operators. Investors areencouraged to keep an eye on this sothey are aware of what types of fraudand scams are being tried.

Typically, investors should be especiallywary if they feel under pressure tomake a decision to invest quickly (suchas a time-limited offer), or are offeredreturns on their investment that soundtoo good to be true, or are told aboutproducts or services that don’t adequatelyexplain the risk of losing money.

CFD trading is inherently speculative,and firms must uphold their responsibilityto warn their clients that their capitalis at risk. Aggressive cold-calling tacticseither by phone, email, online pop-ups,or on social media are also likely to beperpetrated by unscrupulous providersrather than by reputable players inthe market. In the past, we have alsoobserved cases where people have fraudulentlypresented themselves as CySEC representatives in an effort to defraudinvestors. For this reason, CySEC hasissued several announcements informingthe public that it never sendsunsolicited correspondence to investorsor members of the public, nor does itever request any personal data, financialor otherwise.

As we move into a more digitalAs we move into a more digitalworld, the number of risks toinvestors is growing constantly.This is not only due to platformrelatedfraud or illicit activity, butalso due to hacking and cybersecurity.Does CySEC take cybersecurityinto account when auditingregulated firms that use investorsdeposits or accounts? Will you bedoing this in the future?

Data security is an organisationalrequirement under the investmentlaw. CIFs must have sound securitymechanisms in place to guarantee thesecurity and authentication of the meansof transfer of information, minimise therisk of data corruption and unauthorisedaccess, and prevent information leakagein order to maintain the confidentialityof the data at all times. It’s part of CySECsupervisory action plan each year.

What are your plans for theWhat are your plans for thenearest six months? What to expectfrom CySEC?

Our goal as CySEC is to continueacting as a protective shield for investorsthrough effective supervision andguiding the sound development of thesector. As part of our mission we areincreasing the level and the frequencyof supervision, particularly of online tradingplatforms, by expanding our internalresources. Given the internationaland largely web-based nature of theactivities of CIFs, CySEC has acquired asupervisory system for monitoring thesupervised entities’ online marketingactivities/materials. This tool will thereforefurther enhance CySEC’s ability tocollect, analyse, and monitor the marketingcommunications of CIFs. In terms ofpolicy making our aim is to consult onenhancing the clients’ money rules bymid to late 2022.

In addition, we have received fundingapproval from the EU Recoveryand Resilient Fund to explore the opportunityof transforming our InnovationHub into a Regulatory Sandbox. In thiscontrolled environment, fintech startupsand other entities will be able to testtheir innovative products or servicesin real conditions under the regulator’ssupervision.

We are also launching the Trust RegisterPortal which will keep the details ofthe beneficial owners of express trustsand similar legal arrangements. ThePortal is an additional tool to improvetransparency and combat money launderingand terrorist financing.

CySEC is also introducing new examsfor the providers of financial informationin regulated entities as part of the financialeducation of industry professionalsto ensure a high standard of service.

In 2020, CySEC added a newIn 2020, CySEC added a newregulatory category, Mini Managers,and a new investment product,Crowdfunding. What has beenthe reaction to these so far? Isthere scope to introduce other newregulatory categories?

Although the initial reaction has beenAlthough the initial reaction has beenfairly slow, we have recently approvedthe licence of the first mini managerand also pre-approved the licence of thefirst crowdfunding platform. Once thesenew entities start operating, and if theyend up being successful, I do see a trendtowards more applications in the futurefor both mini-manager and crowdfundingplatforms.

CySEC is also introducing a newregulatory category for fund administrators.The draft law will be submittedto the Ministry of Finance in 2022. Thefund administration is not regulatedat EU level; however, we believe thatregulating these entities will contributeto enhancing investor protection andmarket integrity by ensuring authorisationand supervision throughout thedelegation chain.

We are also looking at loan originationand loan participation for the fundsindustry. In many countries, there arerestrictions on these so we are beingcautious to make sure we address therelevant risks.

Environmental, social and governance-Environmental, social and governance-related factors are rapidlybeing integrated into the institutionalframework of the capitalmarkets. How ready are the regulatedentities to adopt the specificcriteria?

As in the case of any new regulation notonly in Cyprus but at EU and global level,we expect that there will be challengesin the application of ESG until a level ofmaturity is reached. Market participantsand investors are not fully informedabout what ESG entails and while someregulations have been passed in Europe,there's still no uniformity of regulatorypractices and approaches. There is alwaysthe risk of greenwashing or mislabellinginvestments towards ESG. If you havean investment that labels itself as ESG,somebody needs to approve it, somebodyneeds to rate it, but the criteria for thisare not clear yet. More work needs to bedone at national and EU level to createsustainable growth in this market.

In Cyprus, although we are yet to seeIn Cyprus, although we are yet to seea large-scale shift towards responsibleinvestments, we have already signed upa few alternative investment funds withan investment policy focusing on ESGfactors. Data gathered from asset managersin Cyprus showed that €40.2 millionof funds under management have asustainable investment strategy, whichis indeed a very promising step in theright direction. To encourage and assistinvestors and regulated entities in thisregard, and in line with the EU actionplan for financing sustainable growth,CySEC has confirmed its commitmentto fostering compliance with sustainablefinance standards, and in early 2021 wecreated a dedicated section on our websiteon sustainable finance, which givesinformation on the legislative measuresbeing introduced at the EU level.

Dr George Theocharides

Chairman of the Cyprus Securities and Exchange Commission (CySEC)

Dr Theocharides served as CySEC’s Vice Chairman since July 2020 andwas appointed new Chairman in 2021. As an Associate Finance Professor atthe Cyprus International Institute of Management (CIIM) and Director of theMSc in Financial Service Programme from September 2010 until July 2020, hehas extensive work experience in the wider financial sector.

Dr Theocharides served as CySEC’s Vice Chairman since July 2020 andwas appointed new Chairman in 2021. As an Associate Finance Professor atthe Cyprus International Institute of Management (CIIM) and Director of theMSc in Financial Service Programme from September 2010 until July 2020, hehas extensive work experience in the wider financial sector.

Prior to joining CIIM, he worked as an Assistant Professor of Finance atthe Sungkyunkwan University of South Korea and as an International FacultyFellow at the Sloan School of Management of the Massachusetts Institute ofTechnology (MIT).

In the past, he served as a member of the Board of the Cyprus Securitiesand Exchange Commission, a member of the Interim Board of Bank of Cyprus,Chairman of the Board of the Cyprus Blockchain Technologies Ltd, as well as amember of the Board of Directors of the Cyprus-Kuwait Business Association.He also served as a member of the Training/HR Committee of the CyprusInvestment Funds Association (CIFA), as well as a non-executive member of theBoard of Directors for a number of organisations and companies in the financialservices sector.

He is also an Associate member of the Chartered Institute forSecurities & Investment (CISI) and a Research Associate at the UCL Centre forBlockchain Technologies (UCL CBT).

Dr Theocharides holds a degree of BEng (Hons) in Electrical Engineering &Electronics from the University of Manchester (U.M.I.S.T.), an MBA from theUniversity of San Diego, and a PhD in Finance from the University of Arizona.

Today more than ever, wealthy families are faced with new risks, challenges, and changing needs both for the business and the family. Family Offices are evolving to meet these needs:

Protect the family wealth through effective asset protection, investment management, and succession planning.

Enhance family cohesion and transition between generations regarding the family’s legacy, strategy, values, and key decisions.

Exercise better control over family holdings/assets through the right governance.

Manage the various risks facing the family (including investment risk, reputation risk, etc.) by proactively preparing for various eventualities.

Manage all aspects of family needs and affairs, by providing the relevant support and alleviating administration burden.

PWC: WHY DO PEOPLE CREATE FAMILY OFFICES?

The rapidly transforming socioeconomic scenery, increasing complexity, scrutiny, and new regulatory requirements are some of the reasons why many wealthy families set up their own Family Office to better control their wealth and handle their private affairs. Since every family has its own unique set of circumstances, there are as many types of family offices as there are families. Some provide administrative support while others oversee the management of investments and coordinate all of the family's financial and personal/lifestyle needs.

K. TREPPIDES & CO: SUCCESSION PLANNING AND NEXT GENERATION – WHAT IS THE DANGER?

The ideal scenario for a family business is to continue to grow for future generations without any difficulties. However, it might be difficult to find the right successor within the family to lead the business into the future.

NEXT GENERATION

The next generation might not be interested in a position within the family office or might not have the capabilities to lead the office after the current generation steps down. However, it might also be the case that some of the youngest family members are willing and capable to take over the family office functions, but at the end there can only be one prevailing chief executive officer.

On the contrary, non-family members might be better qualified to take over the role and therefore to run the business in a more efficient and effective way.

IMPLIED RULE OF 92%

The rule states that the 92% of a family’s wealth is lost by the third generation. The main reason behind this is that families tend to focus merely on ‘hard needs’ (such as business operations, investment strategy, and assets allocations) at the expense of recognising the importance of ‘soft needs’ (such as succession planning, philanthropy, and the responsibilities associated with having access to such vast sums of wealth).

Historically, having a poorly implemented succession plan, or no succession plan, can contribute significantly to families losing almost all their wealth by the third generation. To prevent this, the establishment of a family office has an implacable role to prove that the said rule is wrong.

The submission of data concerning beneficial ownership is due by 12 March 2022 in accordance with the relevant announcement of the Department of Registrar of Companies and Intellectual Property.

LEGAL BACKGROUND

In early 2021, the Cyprus government transposed the 5th EU Anti-Money Laundering (AML) Directive into Cyprus legislation, amending the Law for the Prevention and Suppression of Money Laundering Activities.

Consequently, all companies and other legal entities that are incorporated or registered in the Republic of Cyprus are now obliged to identify and record onto the Beneficial Ownership (BO) Register all relevant information about their beneficial ownership.

DEFINITION OF BENEFICIAL OWNER

In accordance with the law, a beneficial owner is defined as any natural person(s) who ultimately owns or controls the Obliged Entity and/or the natural person(s) on whose behalf a transaction or activity is being conducted and includes at least:

a. for corporate entities: the natural person(s) who ultimately owns or controls a legal entity through direct or indirect ownership of a sufficient percentage of the shares or voting rights or ownership interest in that entity, including through bearer shareholdings, or through control via other means. A shareholding of 25% plus one share or an ownership interest of more than 25% in the customer held by a natural person shall be an indication of direct ownership.

b. for trusts: the settlor; the trustee(s); the protector, if any; the beneficiaries, or where the individuals benefitting from the legal arrangement or entity have yet to be determined, the class of persons in whose main interest the legal arrangement or entity is set up or operates and any other natural person exercising ultimate control over the trust by means of direct or indirect ownership or by other means.

c. for legal entities such as foundations and legal arrangements similar to trusts: the natural person(s) holding equivalent or similar positions to those referred to in point (b) above.

OBLIGED ENTITIES

Entities considered as ‘obliged entities’ are the following:

• Companies incorporated or registered under the Companies Law Cap. 113

• European Public Limited Liability Companies Based on a legal opinion recently obtained from the Attorney General’s Office, partnerships are considered to be legal entities and as such they must disclose BO details in the register. This will be implemented with system amendment for which a relevant announcement will be published by the Registrar of Companies in due course.

The Directive does not apply to the following entities:

• Companies listed on a regulated market that is subject to disclosure requirements consistent with EU law

• Companies whose directors submitted an application for strike off pursuant to Article 327 (2A) (a) of the Companies Law, prior to the commencement of the Directive (12 March 2021)

• Companies whose liquidation has been enacted before the commencement of the Directive (12 March 2021)

• Overseas companies (branches).

All entities whose strike off or liquidation has been enacted after 12 March 2021 are obliged to record the details of their beneficial owners in the BO Register.

The law also provides for the creation of a BO Register for trusts. The information to be entered in the register shall include the identity of the settlor, the trustee, the protector, the beneficiaries and any other natural person exercising effective control over the trust. The information will not be accessible to the public, but it can be accessed only by competent regulators or supervising authorities. This register shall be maintained by the Cyprus Securities and Exchange Commission (CySEC); however, no official guidance has been issued yet.

Full version of this article is available at www.cy.andersen.com

Паромное сообщение с Европой восстановится весной 2022 г. Статистика от Cystat. В кипрских банках растет количество депозитов и снижается доля заемных средств.

28 января 2022 г. закончился срок подачи заявок на создание пассажирского морского сообщения между Кипром и Грецией. 25 ноября 2021 г. был объявлен тендер. К участию в конкурсе проявили интерес нескольких компаний. “Представленные тендерные заявки будут рассматриваться в соответствии с положениями законодательства”, - говорится в сообщении Подминистерства шипинга.

Руководитель ведомства Василис Димитриадис заявил, что “мы пока не празднуем победу, но считаем это важным шагом. Интерес компаний к проекту объясняется пересмотром условий контракта, переработкой тендерной документации и, главное, увеличением субсидии от ЕС для исполнителя контракта. Ожидается, что победитель, выбранный из трех кандидатов, будет объявлен в период с конца февраля по начало марта 2022 г. Паромное сообщение, по предварительным оценкам, начнется в апреле или мае 2022 г. Что касается порта отправления с Кипра, который будет использоваться для паромного сообщения, то это будет зависеть от оператора-победителя”, - сказал В. Димитриадис.

***

Депозиты в кипрских банках на конец 2021 г. составили 51,52 млрд. евро, говорится в отчете ЦБ Кипра, опубликованном 28 января 2022 г. Эти цифры свидетельствуют об увеличении депозитов на 3,31 млрд. евро по сравнению с декабрем 2020 г. Общий объем кредитов на конец декабря 2021 года составил 29,9 млрд. евро, что на 870 млн. евро меньше, чем в декабре 2020 г. Данный факт свидетельствует о сокращении доли заемных средств в кредитных портфелях кипрских банков. Ликвидность в банковской системе Кипра на конец 2021 г. составила 21,6 млрд. евро.

Статистическая служба Кипра (Cystat) объявила в пятницу, что уровень промышленного производства в ноябре 2021 г. достиг самого высокого уровня за 11 лет. Согласно отчету, индекс промышленного производства вырос до 132,6 единиц, зафиксировав рост на 4,4% по сравнению с ноябрем 2020 г. За период с января по ноябрь 2021 г. индекс увеличился на 7,8% в годовом исчислении. По данным Cystat, в ноябре 2021 г. в производственном секторе зафиксирован рост на 5,1%, по сравнению с ноябрем 2020 г. Увеличение наблюдалось в секторе добычи полезных ископаемых (8,3%), а также водоснабжения и утилизации отходов (8,2%).

По материалам cyprus-mail.com

Несмотря на рост интереса к пассивным вложениям через инвестиционные фонды, на локальном кипрском рынке все еще ограниченное предложение для подобных стратегий инвестирования. Журнал “Успешный Бизнес” встретился с CEO и исполнительным директором Андреем Наруцким (АН), управляющим активами Михаилом Борисовым (MБ) и руководителем отдела развития бизнеса Димитрисом Николау (ДН). Представители компании рассказали о своих продуктах и о том, как они могут улучшить предложение для осведомленных и профессиональных инвесторов.

Являясь компанией, созданной на Кипре, какой вы видите роль LEON на локальном рынке?

АН: Мы начинали свою деятельность в качестве мультисемейного офиса в 2013 году. За прошедшие годы у нас накопился большой опыт в управлении капиталом. Мы инвестируем в высоколиквидные активы для состоятельных клиентов (UHNWI) на мировых рынках. В наших новых инвестиционных фондах мы стремимся копировать зарекомендовавшие себя успешные стратегии инвестирования (облигации и хедж-фонды). Для нас интересно осуществить это на Кипре в качестве поддержки локальной фондовой индустрии, помочь ее росту. Мы могли бы реализовать наши стратегии в Люксембурге, более устоявшейся юрисдикции для фондов.Тем не менее, мы решили запустить первые фонды на острове, чтобы поделиться нашим опытом.

Расскажите о Ваших фондах.

АН: У нас есть уже три фонда, которые полностью сформированы, и в которые новые подписки не принимаются. Но мы запускаем два новых фонда. Один из фондов предоставляет возможность инвестировать в корпоративные облигации США. Через другой фонд мы инвестируем в диверсифицированный портфель хедж-фондов.

МБ: Глобальный хедж-фонд LEON построен на нашем опыте, накопленном в LEON в течение 3 лет, и на моем личном 10-летнем опыте в стратегиях хедж-фондов. Мы решили сосредоточиться на частных кредитах, так как верим, что в этой области можно получать стабильный доход. Банки уменьшают кредитование после “Базеля III”. А у фондов есть нужное решение, и мы хотим воспользоваться этой возможностью.

Как отличаются стратегии двух фондов?

МБ: В то время как первый фонд инвестирует непосредственно в корпоративные облигации США, хедж-фонд инвестирует в компании, предлагающие кредитование. Как это происходит? Например, компания покупает чужую дебиторскую задолженность со скидкой и, по сути, зарабатывает на этом деньги. Это похоже на стратегию с фиксированным доходом, но прибыль существенно отличается с точки зрения факторов риска и источников получения прибыли.

Для хедж-фонда ключевым фактором является управление риском ликвидности и кредитным риском. Основное внимание уделяется выбору надежных партнеров, проверке всех процедур, информации и согласованию взаимовыгодных условий для наших инвесторов.

Кроме опыта, какие еще гарантии вы можете предоставить людям, доверяющим вам свои деньги?

МБ: Стандартная безопасность, которую могут предложить фонды, обеспечивается соблюдением регуляторных правил. Наша фирма, а также каждый фонд, строго регулируются этими правилами. Для их исполнения, у нас есть комплексная инфраструктура, состоящая из банков-депозитариев, аудиторов, иных контрагентов. В случае с хедж-фондом, большинство стратегий подразумевают, что кредитные договора заключаются с имущественным залогом. С точки зрения кредитного риска, такой подход обеспечивает гораздо более высокий уровень безопасности, чем прямые инвестиции в облигации.

ДН: Я бы сказал, что обе стратегии ранее отсутствовали на локальном рынке. До сих пор существуют инвесторы, которые держат средства в местных банках и получают нулевую прибыль. Мы предоставляем возможность для инвестиций в облигации и на кредитном рынке с хорошо диверсифицированным продуктом, и возможностью получать доходы значительно выше, чем предлагают банки.

Какую конкретную выгоду получат инвесторы от участия в новых фондах LEON?

ДН: Важно отметить профессионализм команды, управляющей средствами. Кроме этого, легкость процесса подписки, управления и инвестирования в эти фонды, а также прозрачность и законодательная защищенность инвестиций.

MБ: Это уникальный продукт, предлагающий инвесторам профиль риска и доходности, который обычно труднодоступен, особенно в хедж-фондах. Обычно минимальный “порог входа” для подобного инвестирования - 1 млн. евро. А формирование диверсифицированного портфеля - 10-15 млн. евро. У нас минимальный “порог” существенно ниже.

АН: У нас серьезный послужной список. Мы построили успешный бизнес по управлению активами. В управлении LEON в настоящее время находится 1 млрд. евро в индивидуальных портфелях. Это результат нашей восьмилетней деятельности. Новое направление в бизнесе мы запускаем на прочной основе уже работающего бизнеса, что является веским аргументом для доверия к нам.

Все фонды, которые мы запускаем, будут иметь стартовый капитал в размере 5-10 млн. евро. Главное преимущество управляющих фондами LEON - это их локальное присутствие на Кипре. Наши управляющие доступны в любое время, и инвесторы всегда имеют возможность связаться с ними для получения актуальной информации об их инвестициях в фонды.

Какой размер капитала будут иметь фонды?

АН: Мы планируем привлечь в каждый фонд 100 млн. евро в течение трех лет.

Фермерство на Кипре становится объектом для инвестирования. Необходимы финансовые и интеллектуальные вложения для: современных систем орошения, солнечной энергетики, развития земледелия в горных районах, цифровизации всех технологических процессов.

Новая стратегия аграрной политики Кипра находится на рассмотрении Еврокомиссии с декабря 2021 г. Стратегия рассчитана на реализацию в течение четырех последующих лет (с 2023 по 2027 гг.) при условии финансирования программы на сумму 461.9 млн. евро. Министр сельского хозяйства Костас Кадис уточнил, что “за период с 2023 по 2027 гг. на реализацию стратегии будет выделено 461.9 млн евро, из которых 83.6 млн. евро поступят из бюджета Кипра, 22 млн. евро - частные инвестиции, а 356.3 млн. евро - это целевое финансирование от Еврокомиссии”.

Костас Кадис рассказал, что “стратегия опирается на девять главных принципов: поддержка эффективных фермерских проектов (земледелие в горных районах, защита сельхозкультур, субсидии сектору животноводства); повышение конкурентоспособности с акцентом на исследования, цифровизацию и технологии производства; оптимизация цепочки поставок продуктов потребителю, продвижение онлайн-торговли фермерскими продуктами; повышение вклада фермерства в борьбу с изменением климата, например, оптимизация управления отходами животноводства и внедрение новых способов по снижению уровней аммиака; продвижение принципов устойчивого развития и эффективного управления естественными ресурсами (водой и почвой); вклад в сохранение биоразнообразия, укрепление экосистем и сохранение мест обитания животных и растений; привлечение новых фермеров в сельское хозяйство и упрощение предпринимательской деятельности в сельскохозяйственных районах; повышение уровня занятости, социальной интеграции и локального развития в сельской местности; повышение эффективности сельского хозяйства с точки зрения запросов общества, продвижение принципов правильного содержания животных на фермах.

Напомним, что в 2021 г. министр Костас Кадис дал интервью журналу “Успешный бизнес”. В частности, министр рассказал о производстве органических продуктов, пользующихся спросом в ЕС и в других странах. Речь шла о сосисках “Цамарелла” и ветчине “Хиромери”, которые получили логотип защищенного географического указания Европейского союза - PGI. Эти две позиции увеличили количество защищенных кипрских продуктов до восьми. Министр надеется, что в ближайшее время в список PGI будет включен кипрский картофель.

По материалам philenews.com