2021 is the year to expect the unexpected. While many trends of the previous years will continue, their path may deviate pressured by unpredicted developments that Covid-19 is causing on the global markets. Let’s have a look at what role vaccine rollouts will be playing in the year ahead, how technology will keep on evolving, and why the new ‘remote’ life will be driving the changes.

VACCINE ECONOMY

The key factor defining how life will be through 2021 is the vaccination against Covid-19. Mass inoculation is, for the time being, the only realistic mean to reduce the need for job- and businessdestroying lockdowns. Led by the UK, the US, Russia and China, the countries around the world are gradually starting their vaccination programmes, but the logistics and distribution remain challenging, especially in remote areas and in low- and middle-income settings.

According to a World Bank Group survey in June 2020, most Cypriot companies did not expect to be hiring their full staff back in the next nine months; now this prospect has been pushed even further into the future. Since the start of a vaccination programme, Cyprus, as well as the majority of the European countries, will need at least six months to see some signs of recovery. The forecasts are that industry will lead the growth, followed by the financial sector. Consumption, on the other hand, will be picking up slower than other sectors, which may inhibit overcoming the economic slowdown.

The EU is likely to have vaccinated 50% of the population no earlier than by May, and may have reached the 70% mark by autumn – assuming that people en masse are convinced about vaccines’ effectiveness and safety, and agree to a jab. This dynamics is important for Cyprus, as a large part of its economy depends on tourism. The country needs people coming from abroad, especially from the EU and the UK, to support local business, but it also needs to protect its population from the disease.

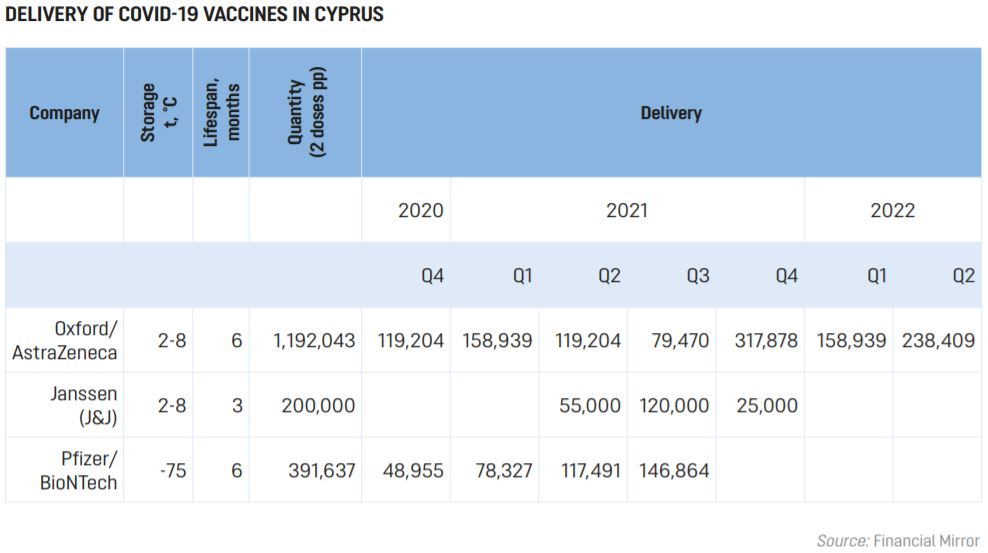

For Cyprus, there is a vaccination programme in place since the end of 2020. As of December 2020, the country ordered around 1.8 million doses, from Oxford/ AstraZeneca, Pfizer/BioNTech and Johnson & Johnson’s Janssen. Negotiations are underway with Sanofi/GSK, Curevac and Moderna. While securing the delivery of the vaccines is an important step, managing the programme will be a challenge for the government in terms of organising the locations for administration, preparing medical staff, launching the necessary IT infrastructure, etc.

According to OECD, if a vaccine is deployed fast, this would boost confidence, spending, and the global GDP growth in 2022. If vaccination proves challenging, the containment measures would be prolonged and uncertainty would deepen. This would further raise the risk of bankruptcies and job losses, limit consumer spending and business investment. Substantial repricing could occur in financial markets, reflecting greater risk aversion. This would weaken global growth, particularly in 2021.

A vaccine has never arrived in the middle of a pandemic before, so there is no historical data for solid predictions. One can be sure, however, that any economic indicators as well as asset prices are tightly linked with either success or failure of the vaccination programme. Any kind of deviation or setback poses a risk of a quick downside for stock markets and house prices.

To be continued